The new math of legal tech investment

Why Legal Tech Funding Is Shifting from Growth to Profitability Metrics

Introduction: The End of Growth-at-All-Costs

For nearly a decade, legal tech investment operated under a simple premise: growth justified everything. Startups that demonstrated explosive user acquisition, rapid revenue expansion, and market share capture attracted legal tech fundingregardless of unit economics, customer retention, or path to profitability. The assumption was that scale would eventually produce profits — and that companies that didn't prioritize growth would be left behind by those that did.

That era has ended. The legal technology investment trends have undergone a fundamental transformation, with investors now demanding evidence of sustainable business models before committing capital. The metrics that once secured term sheets — monthly active users, gross revenue growth, logo acquisition — have been displaced by indicators that predict long-term viability: net revenue retention SaaS, average contract value SaaS growth, implementation success rates, and gross margin trajectory.

This shift reflects the broader shift from growth to profitability in technology investment following the 2022-2023 market correction, but the legal technology sector faces particular pressure. The legal tech market trends that fueled easy funding — AI hype, digital transformation urgency, remote work acceleration — have matured into a market where investors distinguish between genuine value creation and marketing narratives. The capital that once flowed to any company with "AI" in its pitch deck now flows only to companies that can demonstrate customers actually pay for, use, and renew their products.

The implications for legal tech startups funding are profound. Companies that optimized for growth metrics must now optimize for SaaS profitability metrics — a transition that requires fundamentally different strategies, operations, and sometimes business models. The founders who understood that sustainable SaaS growth always mattered are well-positioned; those who assumed growth would eventually justify itself face difficult pivots or extinction.

"The party is over for legal tech companies that confused fundraising with business building," observes a veteran venture capital legal tech investor. "We're no longer funding narratives — we're funding businesses. Show me the retention, show me the margins, show me customers who actually use the product."

— Emily Radford

This analysis examines why the legal tech investment landscape has shifted, what legal tech KPIs now matter for fundraising, and how legal technology companies can position themselves for success in the new environment where investor focus on profitability has replaced the growth-at-all-costs mentality.

Understanding the Funding Environment Shift

The transformation in legal technology funding reflects multiple converging factors that have reshaped investor expectations across the technology sector while creating particular dynamics in legal tech.

The Macro Environment Change

The zero-interest-rate environment that fueled a decade of growth investing ended abruptly in 2022. When capital was essentially free, investors could afford to fund companies that wouldn't produce returns for years — the opportunity cost of patient capital was minimal. When interest rates rose, the calculus changed fundamentally. Capital deployed to unprofitable growth companies now competed against risk-free returns from treasury bonds; the hurdle for venture returns increased accordingly.

The public market correction that accompanied rising rates eliminated the exit path that growth-stage investors had relied upon. According to PitchBook's venture capital analysis, companies that might have gone public at aggressive multiples in 2021 found the IPO window closed; those that did go public often traded down dramatically. The feedback loop that rewarded growth investing — fund growth companies, take them public at high multiples, return capital, raise larger funds — broke when public markets stopped rewarding growth at any cost.

The legal tech venture capital implications were immediate. Funds that had deployed aggressively into legal technology faced markdowns that affected their ability to raise subsequent funds. New investments required higher conviction about near-term returns rather than long-term potential. The investors who remained active in legal tech became dramatically more selective about where they deployed capital. The era of easy money had ended, and the adjustment proved particularly painful for companies built on assumptions of perpetual capital availability.

Legal Tech-Specific Dynamics

Beyond macro factors, legal tech industry trends created sector-specific funding challenges:

The AI hype cycle reached saturation. Every legal tech company claimed AI capabilities; investors learned that "AI-powered" often meant basic automation rebranded for fundraising appeal. The differentiation that AI claims once provided evaporated as the market became crowded with similar messaging. Investors now probe AI claims skeptically, demanding evidence that AI capabilities translate to customer value rather than marketing advantage.

The consolidation wave discussed elsewhere reduced the universe of acquirable companies. Strategic acquirers became more selective; private equity roll-ups reached limits on how many similar companies they could absorb. The exit landscape that growth investors depend upon — eventual acquisition or IPO — became less certain, increasing the importance of companies that could generate returns through operations rather than exits alone.

Customer adoption proved slower than projections suggested. The legal technology adoption that vendors promised during COVID-era urgency often didn't materialize at predicted rates. Law firms remained conservative; corporate legal departments faced budget pressure. The market size was real but the penetration timeline extended, making growth projections that investors had funded appear optimistic.

The New Metrics That Matter

The legal tech KPIs that now determine funding success differ fundamentally from those that prevailed during the growth era. Understanding these SaaS KPIs for legal tech — and what they reveal about business health — is essential for companies seeking capital.

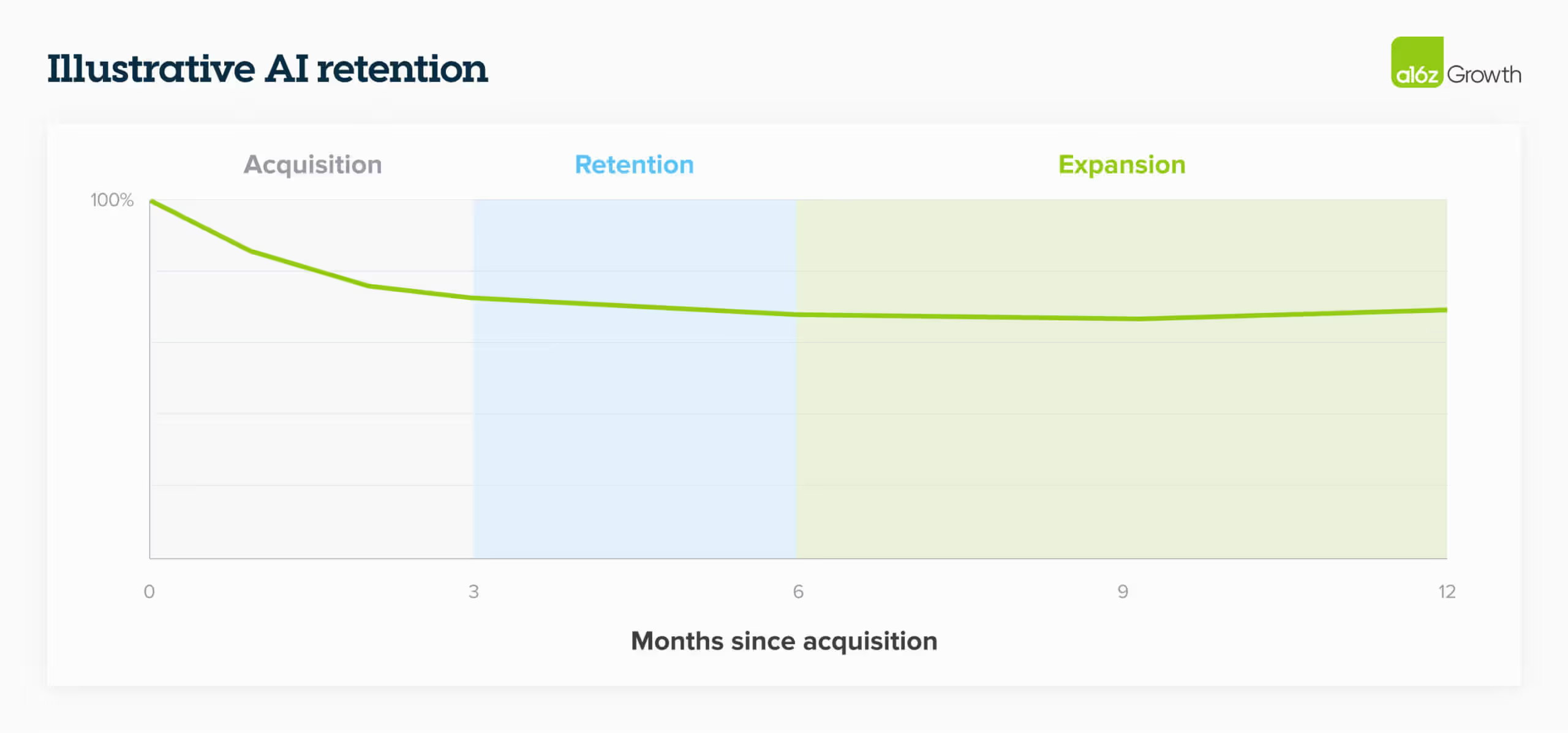

Net Revenue Retention: The North Star Metric

Net revenue retention SaaS (NRR) has emerged as the single most important metric for legal tech investors. NRR measures whether existing customers spend more, less, or the same over time — capturing expansion, contraction, and churn in a single number. An NRR above 100% means the company grows even without acquiring new customers; below 100% means the company must constantly acquire new customers just to maintain revenue.

The focus on NRR reflects hard-learned lessons from the growth era. Companies that grew rapidly through customer acquisition often masked underlying problems: customers who churned quickly, contracts that didn't expand, implementations that failed. Growth metrics looked impressive until they didn't — when acquisition slowed, the weak customer retention legal software foundation became visible.

For legal SaaS metrics, healthy NRR targets vary by segment:

- Enterprise legal tech (large law firms, Fortune 500 legal departments): 110-130% NRR indicates strong product-market fit with expansion potential

- Mid-market legal tech (mid-size firms, corporate legal): 100-115% NRR reflects stable relationships with modest expansion

- SMB legal tech (small firms, solo practitioners): 85-100% NRR acknowledges higher inherent churn in smaller customer segments

Investors now request cohort analysis showing SaaS retention metrics by customer vintage, segment, and product line. Companies that can demonstrate consistent NRR across cohorts signal predictable business models; those with volatile NRR raise concerns about sustainability.

Annual Contract Value and Expansion

ACV SaaS and its growth trajectory reveal whether companies can command premium pricing and expand customer relationships. In legal tech, average contract value SaaS patterns indicate market positioning and competitive dynamics:

Rising ACV suggests pricing power and successful upselling — customers value the product enough to pay more over time and buy additional capabilities. This pattern characterizes companies with strong product-market fit and effective customer success operations.

Flat ACV indicates stable but undifferentiated positioning — customers renew but don't expand, suggesting the product solves a specific problem without creating platform dependency. This pattern can sustain businesses but limits growth potential.

Declining ACV signals competitive pressure or commoditization — customers renegotiate lower prices or downgrade to cheaper tiers. This pattern concerns investors because it suggests weakening market position.

The legal tech unit economics implications of ACV patterns are significant. Investors calculate customer lifetime value (LTV) using ACV and retention assumptions; declining ACV reduces LTV even with stable retention, affecting the economics of customer acquisition investment.

Implementation Success and Time-to-Value

Legal tech implementation success has emerged as a critical investor focus after numerous examples of products that sold well but failed in deployment. The pattern was common: sophisticated enterprise sales teams closed impressive contracts, but implementation teams couldn't deliver promised value, leading to churn that erased the revenue gains. The product adoption metrics SaaS now receive as much scrutiny as sales metrics.

Investors now examine software adoption rate enterprise indicators:

Implementation completion rates — what percentage of signed contracts result in successful deployments versus stalled or failed implementations

Time-to-value — how quickly customers achieve measurable benefits from the product, affecting satisfaction, retention, and reference-ability

Professional services margins — whether implementation services generate profit or represent loss-leader investments that subsidize subscriptions

Customer usage metrics SaaS — actual engagement with the product post-implementation, not just deployment completion

The implementation focus reflects recognition that enterprise SaaS adoption creates obligations, not just revenue. A $500,000 contract that requires $600,000 in implementation cost destroys value regardless of how impressive the logo appears in marketing materials.

Table 1: Legal Tech Investment Metrics — Then vs. Now

| Metric Category | Growth Era Focus | Profitability Era Focus |

| Revenue | ARR growth rate, MRR velocity | Net revenue retention SaaS, gross margin |

| Customers | Logo count, user growth | ACV SaaS expansion, cohort retention |

| Unit Economics | Often ignored | LTV:CAC ratio, payback period |

| Implementation | Contracts signed | Software adoption rate enterprise, time-to-value |

| Profitability | "Path to profitability" narrative | Actual margins, cash flow, burn multiple |

| AI/Technology | AI capabilities claimed | AI driven SaaS metrics, usage data |

Author: Emily Radford;

Source: esmife.com

Why Growth Metrics Failed

Understanding why growth-focused metrics proved inadequate helps explain the shift to profitability focus and guides companies adapting to new expectations.

The Vanity Metrics Problem

Many metrics that impressed during the growth era turn out to measure activity rather than value — what experienced investors call "vanity metrics." These metrics could be optimized without improving underlying business health:

User counts could be inflated through free tiers, trial extensions, and loose definitions of "active" users. A legal tech company might claim 100,000 users while having 5,000 paying customers and 2,000 who actually used the product regularly.

Gross revenue could grow through aggressive discounting that destroyed unit economics. Companies offered multi-year deals at steep discounts to book impressive contract values while committing to unprofitable customer relationships.

Logo acquisition celebrated new customer wins without examining whether those customers succeeded. A company might announce signing a major law firm while knowing the implementation would likely fail and the customer would churn.

The legal tech startup metrics that actually predicted success — retention, expansion, implementation completion, customer satisfaction — received less attention because they were harder to optimize quickly and sometimes revealed uncomfortable truths about product-market fit.

The CAC Payback Trap

The growth era's focus on customer acquisition created a trap that many legal tech companies fell into: spending more to acquire customers than those customers would ever generate in value. The logic seemed sound — acquire customers now, optimize economics later — but the optimization often never materialized.

Customer acquisition cost (CAC) in enterprise legal tech is inherently high. Long sales cycles, multiple stakeholders, security reviews, and procurement processes make each customer expensive to win. When companies prioritized acquisition volume over acquisition efficiency, CAC spiraled while the customers acquired often churned before generating returns.

The legal tech unit economics that investors now examine include:

LTV:CAC ratio — the relationship between customer lifetime value and acquisition cost. Ratios below 3:1 concern investors; ratios above 5:1 suggest room for more aggressive growth investment.

CAC payback period — how long before acquired customers generate enough gross profit to recover acquisition cost. Payback periods exceeding 18-24 months strain cash flow and increase risk.

Gross margin — the percentage of revenue remaining after direct costs. Legal tech gross margins vary by delivery model but typically should exceed 70% for software-dominant offerings; margins below 60% suggest services dependencies that limit scalability.

The AI Hype Discount

AI hype in legal tech contributed significantly to growth-era distortions. Investors funded companies based on AI narratives without verifying that AI capabilities created customer value. The result was a generation of companies with impressive AI demonstrations but limited practical utility. The AI vs SaaS fundamentals debate has resolved firmly in favor of fundamentals.

The hype discount now applied to AI claims means companies must demonstrate AI value through metrics rather than assertions:

AI feature usage — what percentage of customers actually use AI capabilities versus traditional features

AI-attributed outcomes — measurable improvements (time savings, accuracy gains, cost reduction) that AI features produce

AI differentiation — whether AI capabilities create competitive advantage or represent table-stakes features all competitors offer

Investors increasingly view AI as necessary but not sufficient. Generative AI legal tech valuation requires AI capabilities for competitive relevance, but AI alone doesn't justify premium valuations. The companies that command strong valuations demonstrate that AI translates to measurable customer outcomes, not just marketing differentiation. The AI driven SaaS metrics that matter are usage and outcomes, not capabilities claimed.

What Investors Want to See Now

The VC due diligence SaaS process in the current environment focuses on evidence of sustainable, profitable growth rather than growth at any cost. Companies seeking funding must demonstrate specific characteristics that the growth era didn't require. Understanding SaaS investor metrics is now essential for founders.

Path to Profitability (Real This Time)

During the growth era, "path to profitability" was a presentation slide showing projected margins improving over time through scale leverage. Investors accepted these projections without requiring evidence. Now, path to profitability requires demonstrated margin improvement — the profitability vs growth SaaS debate has been settled in favor of profitability.

The legal tech profitability evidence investors seek includes:

Gross margin trajectory — actual improvement in gross margins over recent quarters, showing that scale benefits materialize as promised

Operating leverage — evidence that revenue grows faster than operating expenses, indicating the business model scales efficiently

Contribution margin by segment — profitability analysis by customer segment, product line, or geography showing where the business makes money versus where it subsidizes growth

Cash efficiency — the relationship between cash consumed and ARR growth (the "burn multiple"). Companies burning $2 to generate $1 in ARR face scrutiny; companies burning $0.50 to generate $1 in ARR demonstrate sustainable SaaS growth.

Customer Quality Over Quantity

The shift from logo acquisition to customer quality represents a fundamental change in how investors evaluate traction. SaaS valuation metrics now weight retention and expansion more heavily than new customer acquisition. Quality indicators include:

Customer concentration — reasonable diversification across customers, with no single customer representing more than 10-15% of revenue

Customer segment fit — evidence that the company sells to customers who succeed with the product, not just customers who will sign contracts

Reference-ability — willingness of existing customers to serve as references, participate in case studies, and recommend the product to peers

Expansion velocity — how quickly and consistently customers expand their usage and spending

The legal tech customer success metrics that demonstrate quality include Net Promoter Score, customer effort score, product usage depth, and support ticket patterns. Companies that can show customers actively using and deriving value from products attract investment; those that can only show contracts signed face skepticism. Research from CLOC (Corporate Legal Operations Consortium) confirms that legal technology adoption success correlates strongly with implementation quality and ongoing customer engagement — metrics that venture investors now weight heavily.

Operational Discipline

Investors now evaluate operational discipline as a predictor of management quality and company sustainability:

Hiring efficiency — revenue per employee trends that show the team scales efficiently with growth

Sales efficiency — magic number or similar metrics showing that sales and marketing investment generates proportional returns

R&D productivity — evidence that product development creates customer value rather than feature bloat

Cash management — runway calculations and cash deployment strategy that demonstrate financial responsibility

The legal tech business development approach matters as much as results. Companies that demonstrate thoughtful customer selection, disciplined pricing, and strategic resource allocation signal management teams capable of building sustainable businesses.

"We're looking for founders who understand that raising money is not the goal — building a valuable business is the goal," explains a legal tech-focused venture partner. "The best signal is when founders talk about customer success and unit economics without being prompted. They've internalized that those things matter."

— Emily Radford

Adapting to the New Reality

Legal tech companies seeking funding must adapt strategies, operations, and sometimes business models to meet changed investor expectations. The adaptation requirements vary by company stage and situation.

For Early-Stage Companies

Early-stage legal tech startups face different dynamics than established companies. Investors expect losses during early growth but now scrutinize the efficiency of that growth more carefully:

- Demonstrate product-market fit early — Show evidence that customers need and value the product before scaling sales and marketing investment

- Build retention into the product — Design products that create habitual use and increasing value over time, not just initial utility

- Choose customers strategically — Target customers likely to succeed, expand, and provide references rather than any customer who will sign

- Control burn rate — Extend runway through disciplined spending rather than assuming additional funding will always be available

- Measure what matters — Instrument products and processes to capture retention, engagement, and satisfaction data from the beginning

The legal tech seed funding environment now requires evidence of traction that previous generations of companies didn't need at comparable stages. First-time founders may find this challenging; experienced founders recognize it as a return to fundamentals that should have always applied.

For Growth-Stage Companies

Growth-stage companies face the most difficult adaptation because they may have optimized for metrics that no longer matter while neglecting metrics that now do:

Retention rehabilitation — Companies with weak retention must diagnose causes and implement improvements before seeking additional funding. This may require product changes, customer success investment, or strategic customer culling.

Unit economics repair — Companies with broken unit economics must fix them through pricing increases, cost reduction, customer selection changes, or business model evolution. The repair must be real, not just projected.

Operational rightsizing — Companies that overhired during the growth era must resize organizations to sustainable levels. Layoffs are painful but necessary when headcount exceeds what the business can support.

Narrative reset — Companies that raised on growth narratives must develop profitability narratives that acknowledge past approach while demonstrating new direction. Investors understand pivots; they don't accept denial.

For Late-Stage and Pre-IPO Companies

Late-stage legal tech companies face particular pressure because their path to liquidity depends on public market receptivity that has become more demanding:

Public market readiness — The metrics that public market investors require — consistent profitability, predictable growth, strong retention — must be achieved before attempting IPO

Strategic alternative evaluation — Companies may need to consider M&A or private equity transactions if public market requirements seem unachievable

Investor communication — Existing investors need realistic assessments of timeline and valuation expectations given changed market conditions

Operational transformation — The operational changes required to meet public company requirements are substantial and time-consuming; companies should begin transformation well before anticipated IPO

Table 2: Legal Tech Funding Requirements by Stage

| Stage | Primary Metrics | Investor Expectations | Common Challenges |

| Seed | Early retention signals, product engagement | Clear problem-solution fit, efficient early growth | Demonstrating traction with limited resources |

| Series A | Cohort retention, early unit economics | Repeatable sales process, path to expansion revenue | Proving model works beyond early adopters |

| Series B | NRR >100%, improving gross margins | Scalable operations, segment expansion | Maintaining efficiency while accelerating growth |

| Series C+ | Rule of 40 compliance, profitability path | Operating leverage, market leadership | Transitioning from growth mode to efficiency mode |

| Pre-IPO | Consistent profitability, predictable growth | Public market readiness, governance maturity | Meeting institutional investor requirements |

Author: Emily Radford;

Source: esmife.com

The Private Equity Factor

Private equity legal software investment has emerged as a significant force reshaping the funding landscape. PE approaches differ fundamentally from venture capital, creating alternative funding paths with different requirements and implications. Understanding legal tech M&A trends helps companies evaluate all available options.

How PE Evaluates Legal Tech

Private equity firms evaluating legal tech acquisitions focus on characteristics that venture investors historically underweighted:

Cash flow generation — PE firms often use debt to finance acquisitions, making cash flow essential for debt service. Companies must demonstrate or have clear paths to positive cash flow. The American Bar Association's legal technology surveys show increasing sophistication in how legal organizations evaluate technology investments, aligning with PE expectations for demonstrated value.

Operational improvement potential — PE firms look for inefficiencies they can eliminate to improve margins. Companies with obvious operational improvements are more attractive than those already optimized.

Platform potential — PE firms pursue roll-up strategies combining multiple companies. Acquisition targets that can serve as platforms for additional acquisitions command premiums.

Management quality — PE firms typically retain management through transitions. Teams that demonstrate operational excellence and adaptability are essential for successful PE partnerships.

The legal tech M&A valuations that PE firms offer often differ from venture expectations. PE valuations typically use EBITDA multiples rather than revenue multiples, making profitability directly relevant to valuation rather than just fundability. Enterprise legal software ROI becomes a key evaluation criterion.

PE as Alternative to Venture

For legal SaaS funding that doesn't fit venture profiles — perhaps because they're growing steadily rather than explosively, or because they're profitable but not rapidly scaling — private equity offers an alternative capital source:

Growth equity — PE firms increasingly offer growth capital to profitable companies seeking expansion resources without the hypergrowth expectations of venture capital.

Majority acquisitions — Companies seeking liquidity for founders or early investors can sell majority stakes to PE while retaining operational involvement.

Platform combinations — Companies too small to attract acquisition interest individually may be attractive as additions to PE platforms aggregating related capabilities.

The PE alternative affects venture dynamics by providing competitive capital sources. Companies that might have accepted unfavorable venture terms when VC was the only option now have alternatives that may offer better alignment with their growth trajectories.

Implications for the Legal Tech Ecosystem

The funding shift affects not just individual companies but the broader legal tech ecosystem, reshaping competition, innovation, and market development.

Consolidation Acceleration

The profitability focus accelerates consolidation by making independent survival harder for marginal companies. Companies that can't demonstrate sustainable unit economics face:

Acqui-hire outcomes — Acquisitions valued primarily for team and technology rather than business, with minimal returns for investors

Distressed sales — Acquisitions at valuations below invested capital when companies run out of runway

Shutdown — Companies that can't find acquirers or additional funding simply closing operations

The consolidation benefits well-positioned companies by removing competitors and potentially providing acquisition opportunities for talent and technology. The legal tech market consolidation discussed elsewhere accelerates as funding pressure forces weaker players to exit.

Innovation Implications

The profitability focus raises questions about innovation funding in legal tech. Early-stage innovation is inherently unprofitable; requiring near-term profitability evidence may discourage investment in genuinely novel approaches:

Incremental bias — Investors may favor improvements to existing categories over creation of new categories because incremental improvements show faster paths to profitability

Fast-follower advantage — Companies that copy proven innovations may attract more funding than innovators who create but can't yet monetize new approaches

Corporate innovation shift — Innovation may shift toward corporate R&D at established companies with resources to fund long-term development

However, the counter-argument holds that the growth era funded too much incremental innovation dressed as breakthrough innovation. Companies that couldn't achieve product-market fit kept raising money through narratives rather than results. The profitability focus may actually improve innovation efficiency by forcing faster validation of ideas.

Market Development Effects

The funding shift may affect legal technology adoption rates by changing how companies approach market development:

Slower market development — Companies focused on profitability may invest less in market education and category creation that benefits all players

Premium positioning pressure — Profitability requirements may push companies toward enterprise segments where prices support margins, potentially slowing mass-market adoption

Customer success investment — The retention focus should drive better customer outcomes, potentially accelerating adoption by improving product satisfaction

The net effect on market development is uncertain but the emphasis on customer success and retention should improve the customer experience with legal technology, potentially benefiting adoption even if marketing investment decreases.

Frequently Asked Questions (FAQ)

Why has legal tech funding shifted from growth to profitability metrics?

The shift from growth to profitability reflects multiple factors: rising interest rates that increased the cost of patient capital, public market corrections that closed the IPO exit path, AI hype in legal tech saturation that made differentiation harder, and hard lessons from companies that grew rapidly but couldn't retain customers or achieve profitability. Legal tech investors learned that growth metrics often masked underlying problems — companies looked successful until acquisition slowed and weak retention became visible. The new focus on net revenue retention SaaS, ACV SaaSgrowth, and legal tech unit economics reflects demand for evidence that growth is sustainable and profitable.

What metrics do legal tech investors prioritize now?

Legal tech KPIs now prioritize: Net revenue retention SaaS showing whether existing customers expand or contract over time; Average contract value SaaS trajectory showing pricing power and expansion; LTV:CAC ratio showing unit economics sustainability; gross margin demonstrating scalable business models; software adoption rate enterpriseshowing customers actually achieve value; and burn multiple showing capital efficiency. The SaaS growth vs profitability debate has shifted decisively toward profitability — companies must demonstrate not just revenue growth but profitable, retainable revenue growth.

How should legal tech startups adapt to the new funding environment?

Legal tech startups funding strategies should: build customer retention legal software into products from the beginning rather than assuming they can fix it later; choose customers strategically based on likelihood of success rather than just willingness to sign; control burn rate and extend runway rather than assuming additional funding will be available; measure product adoption metrics SaaS from day one; demonstrate product-market fit before scaling sales investment; and develop realistic financial projections based on actual performance. Companies that internalize SaaS profitability metrics as core operating principles will find funding; those that don't will struggle.

What role does private equity play in legal tech funding now?

Private equity legal software investment has become a significant alternative to venture capital legal tech, particularly for companies that don't fit venture profiles. PE firms focus on cash flow generation, operational improvement potential, and platform value for roll-up strategies. They typically use EBITDA multiples rather than revenue multiples in SaaS valuation metrics, making profitability directly relevant to valuation. PE offers alternatives including growth equity for profitable companies, majority acquisitions for liquidity-seeking founders, and platform combinations for smaller companies. Understanding legal tech M&A trends helps founders evaluate all options.

Will the profitability focus hurt innovation in legal tech?

The venture capital profitability focus raises legitimate concerns about innovation funding — early-stage innovation is inherently unprofitable, and requiring near-term profitability evidence may discourage investment in novel approaches. However, the growth era arguably funded too much incremental innovation dressed as breakthrough innovation; companies that couldn't achieve product-market fit kept raising money through narratives rather than results. The sustainable SaaS growth focus may improve innovation efficiency by forcing faster validation. Additionally, the emphasis on customer usage metrics SaaS and legal tech ROI should improve product quality, ensuring innovations actually create value rather than just attract funding.

Conclusion: The New Normal for Legal Tech Investment

The shift from growth to profitability in legal tech funding represents not a temporary correction but a permanent recalibration of investor expectations. The zero-interest-rate environment that enabled growth-at-all-costs investing is unlikely to return; the lessons learned from growth-era failures will inform investment decisions for the foreseeable future. The legal technology investment trends have fundamentally changed, and companies must change with them.

For legal tech companies, this new normal requires fundamental changes in how they build and operate businesses. The legal tech KPIs that matter — net revenue retention SaaS, ACV SaaS expansion, legal tech unit economics, implementation success — require different strategies than the metrics that mattered before. Companies must build products that customers actually use and expand, not just products that customers sign contracts for. They must price for profitability, not just for competitive positioning. They must succeed with customers they have, not just acquire new customers to mask failures with existing ones.

The discipline required extends beyond metrics to organizational culture. Companies must develop cultures that celebrate customer success rather than just sales wins, that value operational efficiency rather than just growth velocity, that recognize sustainable SaaS growth rather than just impressive headlines. This cultural shift proves difficult for organizations built during the growth era when different values prevailed.

The companies that thrive in this environment will be those that always understood these principles — that sustainable growth requires customer retention legal software excellence, that customer success drives expansion, that legal tech unit economics determine viability. For these companies, the funding shift validates approaches they pursued even when the market rewarded different behavior. They will find legal tech funding because they built fundable businesses.

The companies that struggle will be those that optimized for growth-era metrics without building underlying business health. Some will adapt successfully, implementing the operational changes and strategic pivots necessary to meet new SaaS investor metrics requirements. Others will fail to adapt and will be acquired, merged, or shut down. The legal tech market consolidation that results will ultimately strengthen the sector by concentrating resources in companies capable of building sustainable businesses.

For legal tech investors, the new SaaS KPIs for legal tech provide better signals about company health and investment risk. The investor focus on profitability should improve investment outcomes by filtering out companies that look impressive but lack fundamentals. The investments that succeed under the new criteria should generate returns through operations, not just through optimistic exit multiples. The investor community has learned expensive lessons about what matters; those lessons will inform capital deployment for years to come.

The transition is painful for many participants — founders whose companies don't meet new standards, investors whose portfolios face markdowns, employees whose companies must rightsize. But the destination is a healthier legal tech ecosystem built on sustainable business models rather than perpetual fundraising. That destination benefits everyone who depends on legal technology actually working: the law firms that need reliable tools, the corporations that need enterprise legal software ROI, and the profession that needs technology that creates lasting value.

The new math of legal tech investment is harder than the old math. But it's also more honest — and more likely to produce outcomes that benefit everyone beyond just the participants in the next funding round. The companies that master this new math will define the next generation of legal technology leadership.

Related Stories

Read more

Read more

The content on esmife.com is provided for general informational and educational purposes only. It is intended to present insights, trends, and examples related to investing in legal technology and should not be considered legal, financial, investment, or professional advice.

All information, materials, and references shared on this website are for general informational purposes only. Investment strategies, legal technologies, market conditions, and outcomes may vary based on individual circumstances and should be evaluated independently.

Esmife.com makes no representations or warranties regarding the accuracy, completeness, or reliability of the information provided and is not responsible for any errors or omissions, or for decisions made based on the content presented on this website.