The platform era transforms legal technology competition.

Point Solutions Are Dying: The Rise of Legal Tech Platforms

Introduction: The End of Best-of-Breed

For two decades, the conventional wisdom in legal technology purchasing favored best-of-breed point solutions — selecting the optimal specialized tool for each function and assembling them into a comprehensive technology stack. Document management from one vendor, e-discovery from another, contract management from a third, practice management from a fourth. The theory was elegant: choose excellence in each category rather than accepting compromise from generalist platforms.

That theory is collapsing. The legal tech platform era has arrived, driven by economics that increasingly favor integrated ecosystems over fragmented toolsets. Investors have recognized this shift, redirecting capital from point solution startups toward legal technology platforms capable of capturing broader customer relationships and generating superior unit economics. The market is consolidating around a handful of comprehensive platforms while hundreds of point solutions face existential questions about their futures.

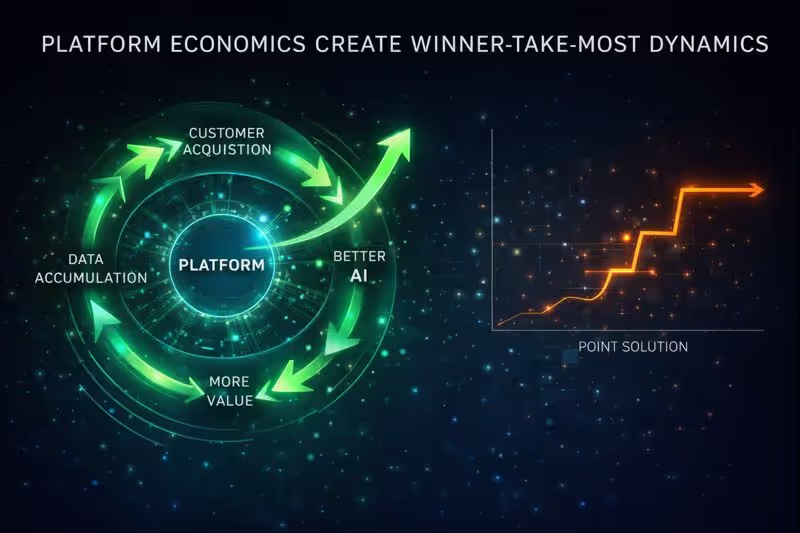

The transformation reflects more than changing buyer preferences — it represents a fundamental shift in how value is created and captured in legal technology. Platform business models legal tech generate compounding advantages that point solutions cannot match: network effects that grow with scale, data advantages that improve AI capabilities, expansion revenue that improves unit economics, and integration depth that increases switching costs. These dynamics create winner-takes-most outcomes where platform leaders capture disproportionate market share and value.

The transition from point solutions to platforms reflects fundamental changes in how legal organizations evaluate and purchase technology. The hidden costs of integration — technical debt, data silos, vendor management overhead, workflow fragmentation — have become impossible to ignore. Legal operations professionals who once championed best-of-breed approaches now advocate for platform consolidation that reduces complexity even at the cost of specialized excellence. The legal tech vendor consolidation they're driving reshapes competitive dynamics across every category.

The legal tech ecosystem transformation carries profound implications for every market participant. Vendors must decide whether to pursue platform ambitions, seek acquisition by platforms, or defend increasingly vulnerable point solution positions. Buyers must navigate a market where their current tools may be acquired, discontinued, or marginalized. Investors must distinguish between platforms positioned to win and point solutions positioned to struggle.

"The point solution era created massive technical debt across the legal industry," observes a chief legal operations officer at a Fortune 100 company. "We had forty-seven different legal tech vendors when I started. We're down to twelve, and the goal is six. Integration is more valuable than optimization."

— Emily Radford

This analysis examines why legal technology ecosystems are winning, how legal tech platform economics reshape competition, and what strategies make sense for vendors, buyers, and investors navigating the platform transition.

Why Point Solutions Are Struggling

The legal tech point solutions that once dominated specific categories now face structural challenges that threaten their viability. Understanding these challenges illuminates why the market is shifting toward platforms.

The Integration Tax

Every point solution in a legal technology stack imposes an integration tax — the cost of connecting that solution to other systems, maintaining those connections, and managing the data flows between them. When organizations operated five or ten point solutions, this tax was manageable. When they operate thirty, forty, or fifty, it becomes crippling.

The legal software integration burden includes:

- Technical integration costs — API development, middleware licensing, custom connectors, and ongoing maintenance as vendors update their systems

- Data synchronization overhead — ensuring consistent data across systems, resolving conflicts, maintaining data quality across boundaries

- Workflow fragmentation — users switching between systems, re-entering data, losing context as work crosses system boundaries

- Security complexity — managing authentication, authorization, and data protection across multiple vendor relationships

- Upgrade coordination — ensuring that updates to one system don't break integrations with others

- Vendor dependency — relying on each vendor's willingness and ability to maintain integration capabilities

The cumulative integration tax often exceeds the value that point solution specialization provides. Organizations discover that the "best" tool for each function creates the worst overall experience when those tools don't work together seamlessly.

The Procurement Burden

Legal technology vendors face increasingly sophisticated procurement processes that disadvantage point solutions. Enterprise buyers have developed vendor management capabilities that recognize the total cost of supplier relationships — not just license fees but implementation, integration, training, support, contract management, and renewal overhead.

Each vendor relationship imposes fixed costs regardless of relationship size:

Security review — every vendor requires security assessment, often including questionnaires, documentation review, and sometimes audits

Contract negotiation — legal review, terms negotiation, and approval processes that consume internal resources

Implementation management — project management, change management, and training coordination

Ongoing administration — license management, user provisioning, support ticket routing, renewal tracking

When these fixed costs apply to a $500,000 platform and a $50,000 point solution equally, the economics favor the platform. The platform delivers more value per unit of procurement overhead, making consolidation rational even when individual point solutions offer superior functionality.

The Data Fragmentation Problem

Point solution architecture creates data silos that limit organizational insight and capability. When contract data lives in the CLM system, matter data in the practice management system, document data in the DMS, and billing data in the financial system, no system has complete visibility into legal operations.

The fragmentation consequences include:

Limited analytics — organizations cannot analyze patterns that span multiple systems without expensive data warehousing and integration projects. The insights that could optimize legal operations remain hidden in disconnected systems.

Incomplete AI training — AI capabilities depend on data access; fragmented data limits what AI can learn and do. Legal AI platform advantages emerge from unified data that trains better models.

Workflow interruption — users must navigate between systems to complete work that crosses boundaries, reducing productivity and increasing error rates

Reporting complexity — management reporting requires manual data combination or custom integration, consuming resources that could create value elsewhere

Compliance challenges — demonstrating compliance requires assembling evidence from multiple sources, increasing audit burden and compliance risk

Knowledge loss — when information lives in disconnected systems, institutional knowledge becomes harder to preserve and leverage

Platforms that unify data across functions can offer capabilities that fragmented point solutions cannot match. The legal tech data integration advantage compounds over time as platforms apply unified data to increasingly sophisticated analytics and AI. The unified legal tech platform value proposition grows stronger as AI capabilities advance.

The Platform Economics Advantage

Legal tech platforms benefit from economic dynamics that create sustainable competitive advantages over point solutions. Understanding these economics explains investor preference for platform investments.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) for selling a comprehensive platform is marginally higher than for selling a point solution — but the revenue from a platform sale is dramatically higher. A sales process that costs $50,000 might yield a $100,000 point solution contract or a $500,000 platform contract. The platform achieves five times the revenue per unit of sales investment.

This efficiency gap compounds through the sales cycle:

Marketing efficiency — platform vendors can address broader audiences with unified messaging rather than narrow category-specific campaigns

Sales productivity — platform sellers address more customer needs per meeting, accelerating deal velocity

Implementation leverage — platform implementations, while larger, achieve better unit economics than multiple point solution implementations

Customer success scale — supporting a $500,000 platform customer costs less than supporting ten $50,000 point solution customers

The legal SaaS platform economics create a flywheel: superior unit economics enable greater sales and marketing investment, which captures more customers, which improves economics further. Point solutions cannot match this flywheel without transforming into platforms.

Expansion Revenue Dynamics

Platform vendors enjoy superior expansion economics through cross-sell and upsell motions that point solutions cannot replicate. A customer using a platform's contract management module represents a warm prospect for document management, analytics, and other capabilities. The trust established through initial engagement reduces friction for expansion sales.

The legal technology platform strategy expansion playbook includes:

Module adoption — selling additional platform capabilities to existing customers at lower acquisition cost than new customer sales

Tier upgrades — moving customers from basic to premium tiers as usage grows and needs expand

Usage expansion — consumption-based pricing that grows automatically as customers use platforms more

Adjacent solutions — extending platforms into related areas (from legal to compliance, from contracts to procurement)

Point solutions have limited expansion paths. A best-in-class e-discovery tool can improve and raise prices, but it cannot expand into contract management or practice management without becoming a platform itself. The expansion ceiling for point solutions constrains their growth potential and thus their value.

Network Effects and Data Advantages

Legal tech ecosystem platforms can develop network effects that point solutions cannot:

Data network effects — platforms with more customers accumulate more data, enabling better AI and analytics, attracting more customers. A contract analytics platform trained on millions of contracts from thousands of customers outperforms one trained on thousands of contracts from hundreds of customers.

Marketplace network effects — platforms that connect legal service buyers and providers become more valuable as both sides grow. More law firms on a platform attract more corporate buyers; more buyers attract more firms.

Integration network effects — platforms with robust integration ecosystems attract partners who build on them, expanding capabilities without platform vendor investment

Standard-setting effects — dominant platforms can establish de facto standards that increase switching costs and attract additional adoption

These network effects create moats that protect platform positions and justify premium valuations. Point solutions lack the scope to develop comparable network effects.

Table 1: Platform vs. Point Solution Economics

| Economic Factor | Platform Advantage | Point Solution Challenge |

| Customer Acquisition | Higher revenue per sales motion | Limited deal size constrains ROI |

| Expansion Revenue | Cross-sell, upsell, usage growth | Expansion ceiling limits growth |

| Retention | Deeper integration increases switching costs | Easier replacement by competitors |

| Gross Margin | Platform scale improves margins | Limited scale constrains efficiency |

| Data Value | Unified data enables AI/analytics | Siloed data limits capabilities |

| Network Effects | Multiple network effect types possible | Scope limitations prevent effects |

Author: Emily Radford;

Source: esmife.com

Investor Perspective: Why Platforms Win

The legal tech investment community has recognized platform economics, shifting capital allocation toward platform opportunities and away from point solution investments. Understanding investor logic helps vendors and buyers anticipate market evolution. The legal tech investor strategy now clearly favors platforms over point solutions across investment stages.

Valuation Premium for Platforms

Legal technology platforms command significant valuation premiums over point solutions in both venture financing and M&A transactions. The premium reflects multiple factors:

Growth potential — platforms can grow through both new customer acquisition and existing customer expansion; point solutions are limited primarily to new customer acquisition

Defensibility — platform integration and data advantages create moats that point solutions lack

Market size — platforms address larger total addressable markets by spanning multiple categories

Exit optionality — platforms can pursue IPO, strategic acquisition, or private equity sale; point solutions primarily pursue acquisition at more modest valuations

Revenue quality — platform revenue typically shows better retention, expansion, and predictability metrics than point solution revenue

The legal tech valuation differential is substantial. A platform growing at 40% annually might command a 15x revenue multiple while a point solution growing at the same rate commands 8x. The gap reflects investor assessment of long-term potential rather than current performance. The platform valuation premium legal tech recognizes the sustainable advantages platforms build.

Roll-Up Economics

Private equity legal tech strategies have recognized that platform value can be created through roll-up — acquiring multiple point solutions and integrating them into unified platforms. This strategy extracts value from point solution fragmentation:

Capability aggregation — combining best-of-breed capabilities into integrated offerings that no individual acquired company offered

Customer consolidation — cross-selling acquired capabilities across combined customer bases, dramatically improving unit economics

Cost synergies — eliminating redundant functions across acquired companies, improving margins

Platform premium capture — achieving platform valuations for what were point solution multiples at acquisition

Management leverage — applying professional management capabilities across multiple product lines

The roll-up opportunity attracts private equity capital that might otherwise avoid legal technology. The strategy requires execution excellence — integration is difficult — but successful execution creates substantial value. Point solution vendors may find PE roll-up their most attractive exit path. According to recent legal tech M&A analysis, deal activity has accelerated as investors pursue platform-building strategies.

The AI Amplifier

AI in legal technology amplifies platform advantages in ways that particularly concern investors evaluating point solutions. The AI capability gap between platforms and point solutions will widen over time:

Data requirements — effective AI requires training data at scales that platforms accumulate and point solutions typically don't. Platforms with millions of documents from thousands of customers train better models than point solutions with thousands of documents from hundreds of customers.

Investment requirements — AI development requires investment levels that platform economics support and point solution economics don't. Building and maintaining competitive AI requires hundreds of millions in investment that point solution revenue cannot support.

Capability expectations — customers increasingly expect AI capabilities as table stakes; platforms can deliver them while point solutions struggle to keep pace with AI-enabled competitors.

Differentiation compression — as AI becomes ubiquitous, the specialized excellence that justified point solutions may be achievable through AI on platforms. The human expertise that point solutions encoded becomes replicable through AI training.

Investors recognize that legal AI platforms represent the future while AI-lacking point solutions represent the past. This recognition redirects capital toward AI-capable platforms and away from point solutions that cannot match AI investment levels. The AI-powered legal tech platform represents the direction of market evolution.

"We don't invest in point solutions anymore unless they're clearly acquisition targets," explains a legal tech-focused venture partner. "The platform economics are just too compelling. Point solutions either become platforms, get acquired by platforms, or slowly decline."

— Emily Radford

How Platforms Are Winning

The legal software platforms capturing market share employ specific strategies that point solutions struggle to counter. Understanding these strategies reveals the competitive dynamics reshaping legal technology.

The Suite Strategy

Leading platforms pursue suite strategies that combine previously separate categories into unified offerings. The legal tech suite approach delivers:

Single vendor simplicity — one relationship, one contract, one integration, one support channel

Unified user experience — consistent interface across functions reduces training burden and improves productivity

Integrated workflows — work flows across functions without system switching or data re-entry

Comprehensive analytics — insights that span functions rather than remaining siloed within categories

The suite strategy particularly pressures point solutions in adjacent categories. When a platform offers "good enough" functionality in a category alongside integration benefits, the point solution's specialized excellence may not justify the integration overhead it imposes.

The Ecosystem Strategy

Platforms complement proprietary capabilities with ecosystem strategies that extend their reach through partnerships:

Integration marketplace — enabling third-party integrations that expand platform capabilities without platform vendor development

API economy — providing APIs that allow customers and partners to build on platform foundations

Partner channel — working with implementation partners, consultants, and resellers who extend go-to-market reach

Developer community — cultivating developers who create extensions, customizations, and complementary solutions

The ecosystem strategy converts potential competitors into complements. A point solution that might compete with a platform capability can instead integrate with the platform, reaching platform customers while accepting a subordinate market position. Research from CLOC (Corporate Legal Operations Consortium) confirms that legal departments increasingly prefer platforms with robust partner ecosystems.

The Land and Expand Strategy

Platforms employ land and expand strategies that begin with focused value propositions and broaden over time:

Land — enter customer relationships with a specific, compelling capability that solves an acute problem

Expand — once established, introduce additional capabilities that address adjacent needs

Consolidate — over time, replace point solutions across the customer's technology stack with platform capabilities

This strategy avoids the "boil the ocean" trap of trying to sell comprehensive platforms before establishing trust. It also creates expansion revenue that improves unit economics over customer lifetime.

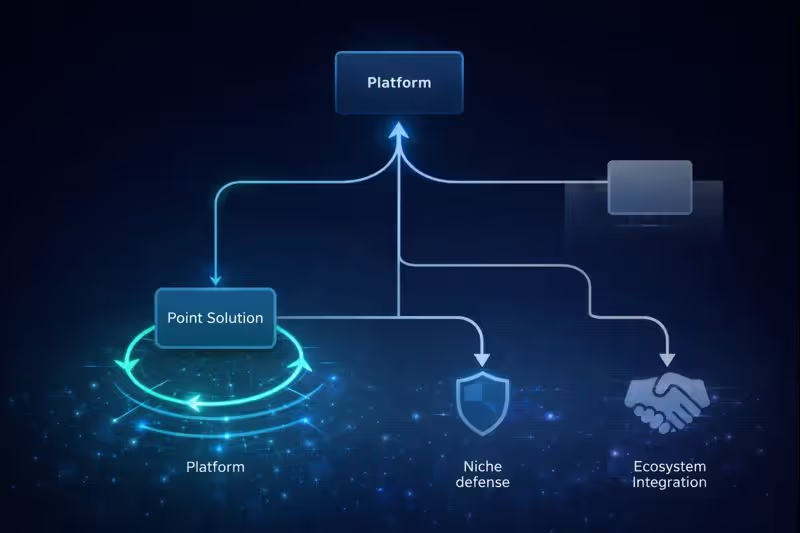

What This Means for Point Solution Vendors

Legal tech vendors operating point solutions face strategic choices that will determine their futures. The options vary based on market position, capabilities, and resources.

Path 1: Platform Transformation

Some point solutions can transform into platforms by expanding scope through development or acquisition. This path requires:

Capital access — platform development requires investment that point solution economics may not support

Execution capability — building or integrating additional capabilities requires skills that specialized teams may lack

Market timing — transformation takes time; the market may consolidate before transformation completes

Customer patience — existing customers must accept transition disruption while the vendor transforms

Platform transformation is the highest-upside but highest-risk path. Success creates a platform competitor; failure may destroy a viable point solution business.

Path 2: Acquisition Positioning

Most point solutions will ultimately be acquired by platforms or platform-building private equity. Legal tech M&Apositioning involves:

Differentiation maintenance — maintaining specialized excellence that makes the point solution attractive for acquisition

Customer relationship quality — building customer relationships that acquirers want to access

Technology architecture — ensuring technology can integrate with acquirer platforms without complete rebuilding

Realistic expectations — accepting that point solution valuations are lower than platform valuations

Acquisition positioning requires balancing near-term business operation with long-term exit optimization. Companies that optimize only for acquisition may underperform operationally; those that ignore acquisition may miss optimal exit windows.

Path 3: Niche Defense

Some point solutions can defend niche positions that platforms choose not to address:

Deep specialization — serving needs so specific that platforms cannot economically address them

Regulatory requirements — meeting compliance requirements that platforms struggle to satisfy

Customer segment focus — serving segments (small firms, specific practice areas, particular jurisdictions) that platforms underserve

Premium positioning — commanding prices that justify specialization for customers who need the best rather than good enough

Niche defense requires realistic assessment of defensibility. Niches that seem protected may prove vulnerable as platforms expand capabilities or acquire niche specialists.

Table 2: Point Solution Strategic Options

| Strategy | Requirements | Upside | Risk | Timeline |

| Platform Transformation | Capital, capabilities, market position | Platform economics, independence | Execution failure, capital exhaustion | 3-5 years |

| Acquisition Positioning | Differentiation, customer quality | Liquidity at reasonable value | Acquirer consolidation, timing | 1-3 years |

| Niche Defense | Deep specialization, customer loyalty | Sustainable independence | Niche erosion, platform competition | Ongoing |

| Ecosystem Integration | Technical capability, partner relationships | Platform reach, reduced competition | Platform dependency, margin pressure | 1-2 years |

Author: Emily Radford;

Source: esmife.com

What This Means for Buyers

Legal technology buyers — law firms and corporate legal departments — must navigate the platform transition with strategies that protect investments and position for future value.

Vendor Viability Assessment

The legal technology procurement process must now include vendor viability assessment that evaluates whether point solution vendors will survive the platform transition:

Financial health — revenue trends, funding status, cash runway that indicate sustainability

Strategic positioning — platform ambitions, acquisition attractiveness, niche defensibility

Customer concentration — dependency on few customers that creates vulnerability

Technology architecture — modern architecture that enables integration and potential acquisition versus legacy systems that don't

Management quality — leadership capable of navigating strategic transitions

Buyers who select point solutions that subsequently fail or degrade face switching costs, implementation disruption, and capability gaps. Viability assessment reduces this risk. The American Bar Association's Legal Technology Surveyprovides benchmarks for technology evaluation.

Platform Evaluation Framework

Buyers evaluating legal tech platforms should assess:

Current capabilities — functionality that meets immediate needs without requiring future roadmap promises

Integration depth — how well platform components work together versus appearing unified but operating separately

Ecosystem health — partner and integration ecosystem that extends platform value

Customer success evidence — reference customers achieving value at scale, not just successful pilots

Roadmap credibility — track record of delivering promised capabilities on reasonable timelines

Exit provisions — data portability and transition rights if the platform relationship ends

The enterprise legal technology evaluation requires more sophistication than point solution evaluation because the stakes are higher and the relationships longer.

Transition Planning

Organizations committed to legal technology stack consolidation should develop transition plans that:

Prioritize high-value consolidation — focus initial efforts on consolidating categories where integration benefits are greatest and point solution excellence is least critical

Manage vendor relationships — communicate consolidation intentions appropriately while maintaining relationships with vendors who may remain in the stack

Preserve institutional knowledge — document configurations, customizations, and workarounds before transitioning away from point solutions

Plan for disruption — budget for productivity impacts during transitions and implementation learning curves

Negotiate strategically — use consolidation intentions as leverage in platform negotiations while avoiding premature commitment

The Emerging Platform Landscape

The legal tech market is consolidating around emerging platform players whose strategies and positioning will shape the industry's future. Understanding the legal tech platform landscape helps stakeholders anticipate competitive evolution.

Platform Archetypes

Several legal technology platform archetypes have emerged, each pursuing platform dominance through different strategies:

Research-anchored platforms — Thomson Reuters (Westlaw) and LexisNexis have expanded from research dominance into adjacent categories, leveraging existing customer relationships and content assets. Their approach involves adding capabilities through acquisition and development while leveraging distribution advantages from research relationships that touch virtually every law firm and corporate legal department.

Workflow-anchored platforms — companies like Relativity have expanded from specific workflow dominance (e-discovery) into broader platform offerings. Their approach builds on deep expertise in specific, high-value workflows and extends that expertise into adjacent areas where similar capabilities and customer relationships provide advantage.

Enterprise software extensions — Microsoft, Salesforce, and other enterprise platforms have added legal capabilities, leveraging existing enterprise relationships. Their approach treats legal as a vertical within broader enterprise platform strategies, potentially leveraging massive existing customer bases and technical infrastructure.

Private equity assemblages — PE-backed roll-ups have combined multiple point solutions into integrated platforms. Their approach involves financial engineering and operational integration to create platforms from previously independent point solutions, capturing platform economics through aggregation.

Native platforms — newer entrants have built platforms from the ground up rather than expanding from point solution origins. Their approach avoids legacy technology debt but requires building customer relationships and capabilities without established market positions.

Each archetype carries distinct advantages and challenges. Research-anchored platforms have relationships but may carry legacy technology debt. Native platforms have modern architecture but lack established relationships. PE assemblages have breadth but face integration challenges. The legal tech platform competition will be determined by which archetypes execute best on their respective strategies.

Competitive Dynamics

The platform competition legal tech will likely produce a winner-takes-most market structure where a small number of platforms dominate while long-tail competitors serve niches:

Enterprise segment — two to four major platforms will likely dominate large law firm and Fortune 500 legal department purchasing. The enterprise segment values integration, breadth, and vendor stability that platform leaders can provide.

Mid-market segment — somewhat more fragmentation may persist as mid-market buyers have less integration complexity to optimize. However, platform economics still favor consolidation as even mid-market buyers recognize vendor management overhead.

SMB segment — potentially different dynamics as smaller organizations may prefer simpler, specialized tools over comprehensive platforms. However, cloud-native platforms increasingly address SMB needs effectively.

The consolidation timeline remains uncertain but directionally clear. The legal tech market consolidation will accelerate as platform economics compound advantages for leaders while disadvantaging point solutions. Organizations should plan for a platform-dominated future while managing current point solution relationships through the transition.

Conclusion: Preparing for the Platform Era

The transition from point solutions to platforms represents a fundamental restructuring of the legal technology market. The economics that once supported hundreds of specialized vendors now favor a handful of comprehensive platforms. The integration tax, procurement burden, and data fragmentation that buyers accepted as necessary costs of best-of-breed strategies have become intolerable as better alternatives emerge.

The platform vs point solution dynamics playing out in legal technology mirror patterns seen in other enterprise software markets — CRM, ERP, HR technology all consolidated from fragmented point solutions to dominant platforms. Legal technology's consolidation follows the same economic logic, driven by the same platform advantages: superior unit economics, network effects, data leverage, and integration value.

For legal tech vendors, the platform era demands strategic clarity. Point solutions that pursue platform ambitions need capital, capabilities, and market timing that many lack. Those that position for acquisition need to maintain value while the market consolidates around them. Those that defend niches need realistic assessment of defensibility. The vendors that thrive will be those that accurately assess their positions and execute appropriate strategies rather than hoping the market reverts to previous dynamics.

For legal technology buyers, the platform era requires procurement evolution. Vendor viability assessment, platform evaluation frameworks, and transition planning capabilities become essential as strategic stakes increase. The buyers that navigate the transition successfully will be those that consolidate strategically, selecting platforms positioned to win while managing relationships with point solutions that may not survive independently. The integrated legal technology future offers genuine benefits — reduced complexity, unified data, better AI — but realizing those benefits requires navigating the transition thoughtfully.

For legal tech investors, the platform era offers clarity about where value will accumulate. Legal tech platform investments command premium valuations because they deserve them — legal tech platform economics create sustainable advantages that point solution economics cannot match. The investors that generate returns will be those that identify platforms positioned for leadership and avoid point solutions positioned for decline.

The point solution era produced genuine innovation and value. The specialization that point solutions enabled drove capabilities forward and served customers well. But the era's fragmentation created costs that integration can eliminate. The platform era will produce its own innovations — enabled by unified data, integrated workflows, and AI capabilities that fragmentation prevented.

The winners of the legal tech platform competition will be those who execute best on platform strategies — whether building platforms organically, acquiring their way to platform status, or positioning as essential platform partners. The losers will be those who deny the transition, hoping that specialized excellence will continue to justify integration overhead that buyers increasingly refuse to accept.

The market is not asking whether platforms will dominate; it is determining which platforms will dominate and how quickly the transition will complete. Organizations across the legal technology ecosystem — vendors, buyers, investors — must position for a platform-defined future. Those that recognize the transition and act accordingly will thrive; those that deny it will find the future arriving whether they're ready or not.

Related Stories

Read more

Read more

The content on esmife.com is provided for general informational and educational purposes only. It is intended to present insights, trends, and examples related to investing in legal technology and should not be considered legal, financial, investment, or professional advice.

All information, materials, and references shared on this website are for general informational purposes only. Investment strategies, legal technologies, market conditions, and outcomes may vary based on individual circumstances and should be evaluated independently.

Esmife.com makes no representations or warranties regarding the accuracy, completeness, or reliability of the information provided and is not responsible for any errors or omissions, or for decisions made based on the content presented on this website.