The monolithic law firm model is fragmenting into specialized components

The Unbundling of Legal Services: Investing in Pieces, Not Firms

For over a century, law firms operated as integrated service providers bundling multiple capabilities under single roofs. A corporation needing legal support engaged a firm that provided everything: research, document drafting, contract negotiation, regulatory compliance, dispute resolution, and strategic counsel. The full-service law firm model bundled these services together, creating institutions that handled diverse legal needs through internal specialization rather than external coordination.

That model is unbundling. The forces that disaggregated other professional services — technology enabling specialization, buyers demanding efficiency, capital funding focused solutions — are now transforming legal services. The unbundling of legal services represents one of the most significant structural shifts in the legal industry, creating investment opportunities in specialized providers that outperform traditional integrated approaches. This legal services market disruption is reshaping how legal work gets done and who captures value from it.

The modular legal services model recognizes that different legal tasks have different characteristics: some are routine and automatable, others require deep expertise; some are high-volume and price-sensitive, others are bespoke and premium-priced; some benefit from scale, others from specialization. Bundling these diverse tasks within single firms creates inefficiencies that specialized providers can eliminate. The legal services unbundling creates opportunities for focused providers to deliver superior solutions for specific needs through legal tech platforms purpose-built for individual modules.

Legal tech investors increasingly recognize the unbundling opportunity. Rather than backing companies attempting to replicate full-service firm models digitally, sophisticated investors target companies excelling at specific pieces of the legal value chain. Investing in legal tech through the unbundling lens means identifying which pieces can be separated, which separations create value, and which specialized providers will capture that value. The legal tech investment opportunities lie in modular legal tech specialists, not integrated generalists.

The unbundling thesis applies across the legal value chain: legal research software that outperforms generalist attorney research; contract drafting software that produces documents faster than traditional drafting; compliance technology legal solutions that monitor obligations more comprehensively than manual tracking; dispute resolution technology that resolves conflicts more efficiently than litigation. Each piece represents distinct investment opportunity with distinct dynamics.

The parallel to other professional services is instructive. Financial services unbundled into payments, lending, wealth management, and insurance — each now addressed by specialized fintech providers. Healthcare services unbundled into diagnostics, treatment, monitoring, and administration — each with specialized technology solutions. Legal services are following the same pattern, with legal tech startups building focused solutions for specific legal needs rather than attempting to recreate integrated firm models. The legal industry transformation follows patterns proven in adjacent sectors.

The investment opportunity is substantial. The global legal services market exceeds $900 billion annually, with significant portions addressable by technology-enabled specialized providers. As unbundling proceeds, value shifts from integrated institutions to focused specialists — and investors positioned for this shift capture returns as transformation unfolds. Understanding the future of legal services requires understanding how legal tech business models are capturing value that law firms once monopolized.

"We stopped asking 'who's building the next great law firm platform' and started asking 'who's building the best contract AI, the best research tool, the best compliance system,'" explains a legal tech investor. "The unbundling thesis changed how we evaluate opportunities. The specialists win."

— Emily Radford

This analysis examines how legal services unbundling is reshaping the market, which pieces create the most value, and how investors should approach the modular legal future.

Understanding Legal Services Unbundling

The unbundling legal services phenomenon follows patterns seen in other industries. Understanding the unbundling dynamic illuminates investment implications.

What Unbundling Means

Unbundling occurs when integrated offerings disaggregate into specialized components that customers can purchase separately. In legal services, unbundling means:

Service separation — legal tasks historically performed together within firms become available from separate, specialized providers

Specialization depth — providers focusing on single tasks develop deeper expertise than generalist firms maintaining breadth

Technology enablement — technology allows specialized providers to deliver services at scale and efficiency impossible for generalists

Buyer optionality — legal buyers can assemble best-of-breed solutions rather than accepting bundled offerings from single providers

According to analysis of unbundling in business strategy, disaggregation creates value when integrated offerings contain components with different optimal delivery models. Legal services fit this pattern precisely.

Why Legal Services Are Unbundling Now

Multiple forces drive legal industry unbundling:

Technology maturation — AI, automation, and cloud platforms enable specialized legal technology that couldn't exist a decade ago. Legal tech platforms can now deliver specific services at quality and scale that justify separation from integrated firms.

Buyer sophistication — corporate legal departments increasingly employ legal operations professionals who evaluate services analytically. These buyers recognize when specialized providers outperform bundled firm services and have authority to engage specialists.

Cost pressure — legal spending scrutiny creates demand for efficient alternatives to premium firm billing. Specialized providers offering better economics for specific tasks attract cost-conscious buyers.

Talent preferences — legal professionals increasingly prefer specialized roles in focused companies over generalist careers in traditional firms. Talent flows to specialists, enhancing their capabilities.

Capital availability — venture capital funding specialized legal technology companies enables growth that creates viable alternatives to firm-delivered services.

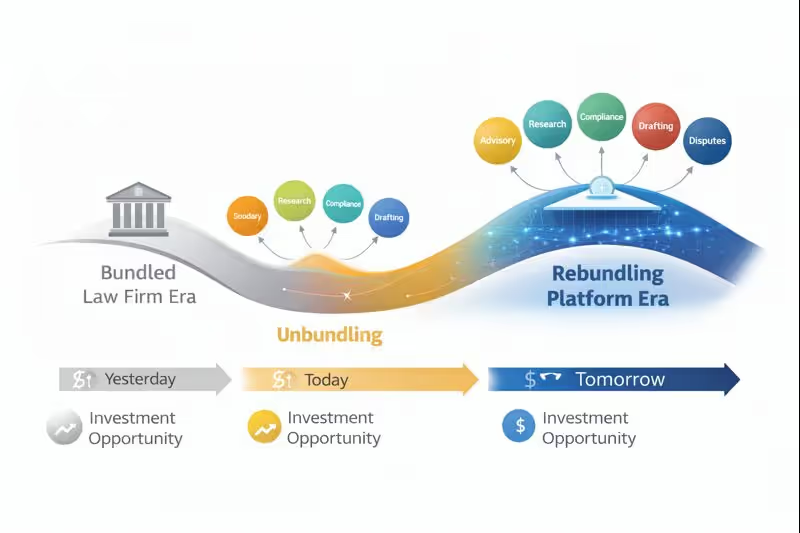

The Bundling-Unbundling Cycle

Legal services are mid-cycle in the bundling-unbundling dynamic that characterizes many industries:

Historical bundling — law firms bundled services because coordination costs exceeded transaction costs of internal delivery. Firms provided research, drafting, advice, and representation together because coordinating external specialists was impractical.

Current unbundling — technology reduces coordination costs while enabling specialists to achieve scale. Transaction costs of engaging specialists have fallen below coordination costs of internal bundling, driving disaggregation.

Future rebundling — eventually, platforms may rebundle specialized services into integrated offerings. But the rebundling will occur on different foundations than traditional firms, likely with technology platforms coordinating specialized providers rather than partner-led institutions.

Investors positioning for the unbundling phase capture value as disaggregation proceeds. Those who also anticipate rebundling dynamics can position for subsequent consolidation.

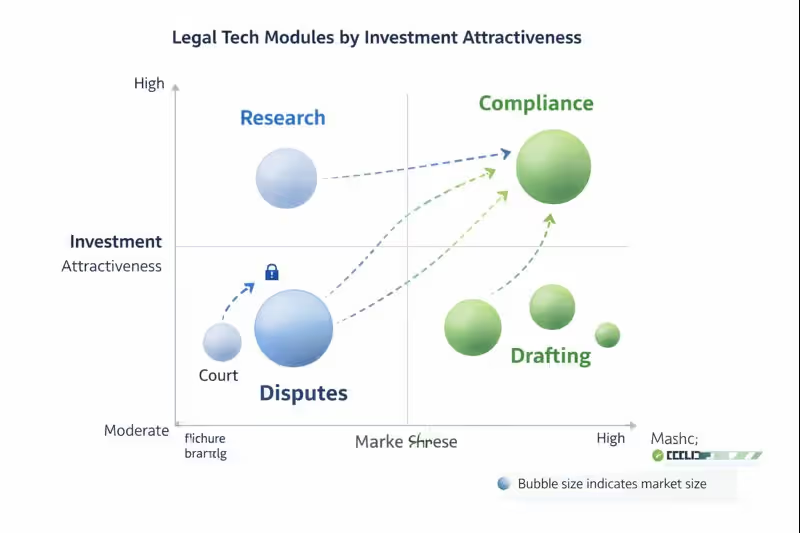

The Modular Legal Services Map

Understanding which legal service modules are separating and where value concentrates guides investment focus. The modular legal tech landscape comprises distinct categories with different dynamics. This legal tech market analysisexamines each major module.

Legal Research Module

Legal research software represents one of the most developed unbundled categories:

Traditional model — law firm associates conducted legal research, billing hours for work that varied widely in efficiency and quality

Unbundled model — specialized AI legal research tools powered by advanced NLP deliver faster, more comprehensive research than manual attorney work. These legal service platforms provide instant access to relevant precedents, statutes, and analysis.

Market leaders — established players and AI-powered entrants compete to deliver superior research capabilities through legal knowledge management software

Investment dynamics — the category is maturing, with consolidation likely. Investment opportunity shifts toward next-generation AI research capabilities and vertical SaaS legal tech solutions for specific practice areas.

Legal research AI has demonstrated that specialized providers can outperform generalist firm capabilities. Research unbundling validates the broader thesis while illustrating category evolution patterns.

Legal Drafting Module

Legal document drafting software and automated legal drafting represent substantial unbundling opportunity:

Traditional model — attorneys drafted documents manually, adapting precedents and creating bespoke content regardless of complexity or standardization potential

Unbundled model — contract drafting software and document automation platforms generate initial drafts, standard documents, and even complex instruments with human review

Market segments — the category segments by document type: contracts, litigation documents, corporate filings, regulatory submissions. Each segment has distinct dynamics and legal SaaS business model characteristics.

Investment dynamics — AI contract drafting is rapidly advancing with generative AI. Early-stage investment opportunity remains significant in segments where AI can augment or replace manual drafting. These represent scalable legal tech opportunities with strong recurring revenue legal software models.

The drafting module illustrates how unbundling creates tiered service models: AI handles routine drafting, specialists handle complex drafting, and firms retain only the most bespoke, strategic document creation.

Compliance Module

Compliance technology legal represents high-growth unbundled category:

Traditional model — law firms provided compliance advice and monitoring as part of broader regulatory practices, often reactively

Unbundled model — regulatory compliance software provides continuous monitoring, automated alerts, and proactive legal compliance automation that firm-based approaches cannot match. Compliance management platforms deliver capabilities at scale.

Market drivers — regulatory complexity increasing across industries drives demand for specialized compliance solutions. Manual approaches cannot scale to monitor expanding obligations. Governance risk compliance softwareaddresses enterprise needs comprehensively.

Investment dynamics — compliance tech attracts significant investment due to large addressable markets and clear ROI demonstration. The category extends beyond pure legal into broader GRC (governance, risk, compliance).

RegTech and compliance automation illustrate how unbundling creates new categories that didn't exist in traditional firm models. Firms never provided continuous automated compliance monitoring because the technology didn't exist; now specialized providers deliver capabilities firms cannot replicate.

Dispute Resolution Module

Dispute resolution technology is unbundling litigation and arbitration:

Traditional model — law firms handled disputes from inception through resolution, bundling investigation, strategy, document production, motions, discovery, trial, and settlement

Unbundled model — specialized providers address specific dispute phases: e-discovery platforms for document production, AI litigation analytics for case assessment, online dispute resolution platforms for case resolution

Market segments — dispute tech segments by phase, case type, and forum. Consumer disputes, commercial arbitration, and complex litigation each have distinct unbundling patterns.

Investment dynamics — litigation management software investment varies by segment. E-discovery is mature; ODR is growing rapidly; legal case management software is evolving with AI. Alternative dispute resolution technology for arbitration and mediation represents emerging opportunity.

The dispute module shows how unbundling can occur at multiple levels — entire categories (dispute vs. transactional) and sub-phases within categories (discovery vs. trial preparation).

Contract Lifecycle Module

Contract lifecycle management (CLM) represents major unbundled category:

Traditional model — firms drafted contracts and provided negotiation support; companies managed executed contracts manually or through basic systems

Unbundled model — CLM platforms manage entire contract lifecycles: creation, negotiation, execution, obligation tracking, renewal management, analytics. Enterprise legal management software integrates CLM with broader legal operations.

Market position — CLM has achieved significant market penetration and represents one of legal tech's largest categories by revenue

Investment dynamics — contract management software market is maturing with consolidation underway. Investment opportunity shifts to AI enhancement, vertical specialization, and integration plays.

Contract AI and contract analytics represent CLM's evolution, adding intelligence to workflows that earlier generations managed operationally.

Table 1: Legal Services Module Comparison

| Module | Unbundling Maturity | Market Size | Growth Rate | Key Investment Thesis |

| Legal Research | High | $3-5B | 8-12% | AI enhancement, next-gen platforms |

| Legal Drafting | Medium | $2-4B | 15-25% | Generative AI transformation |

| Compliance | Medium-High | $8-15B | 20-30% | Regulatory complexity driver |

| Dispute Resolution | Medium | $4-8B | 12-18% | ODR growth, AI analytics |

| Contract Lifecycle | High | $5-8B | 15-20% | AI enhancement, vertical expansion |

Author: Emily Radford;

Source: esmife.com

Why Pieces Beat Integrated Providers

The unbundling investment thesis rests on the proposition that specialized providers outperform integrated alternatives. Understanding why pieces beat whole informs investment strategy.

Specialization Advantages

Specialized legal tech providers enjoy structural advantages:

Depth over breadth — specialists develop deeper expertise in their domains than generalists maintaining broad capabilities. A company focused solely on contract AI develops better contract AI than a company building contract features alongside many other capabilities. The difference compounds over time as specialists accumulate domain knowledge that generalists cannot match.

Talent concentration — specialists attract talent passionate about their specific domain. The best legal AI engineerswant to work at focused AI companies, not at generalist legal platforms where their domain is one of many features. This talent concentration creates capability advantages that reinforce market position.

Customer intimacy — specialists develop deep understanding of customer needs in their specific domain. They observe edge cases, understand workflows, and anticipate needs that generalists miss. A compliance software specialist understands compliance officer workflows intimately; a generalist providing compliance alongside other features understands workflows superficially.

Iteration speed — specialists iterate faster in their domains because all development resources focus on single problems. Generalists allocate development across many areas, slowing progress in each. Legal tech product development velocity advantages compound as specialists ship improvements while generalists balance competing priorities.

Market positioning — specialists can position as best-in-class solutions for specific needs. Generalists position as "good enough" across many needs, losing competitive positioning to specialists everywhere. Legal tech marketing for specialists is clearer and more compelling than generalist messaging attempting to address diverse audiences.

Customer success focus — specialists can invest deeply in customer success for their specific use case. Generalists spread customer success resources across diverse use cases, providing shallower support everywhere. Legal tech customer success at specialists creates retention advantages that compound through expansion and referral.

Unit Economics Advantages

Modular legal tech often exhibits superior unit economics:

Focused GTM — specialists can focus go-to-market efforts on specific buyer personas with specific pain points. Legal tech sales efficiency improves when targeting narrow audiences with precise value propositions rather than broad audiences with generic messaging.

Implementation simplicity — specialized products implement faster than integrated platforms, reducing customer acquisition costs and accelerating time-to-value. Legal tech implementation timelines of weeks rather than months improve unit economics significantly.

Reduced complexity — focused products require smaller teams, simpler architecture, and less infrastructure than integrated platforms attempting to do everything. Legal tech startup burn rates at specialists are often lower than at generalists pursuing broader visions.

Pricing power — best-in-class specialists command premium pricing that "adequate" generalists cannot. Buyers pay more for the best solution to specific problems than for mediocre solutions to many problems. Legal tech pricing at specialists can reflect value delivered rather than competing on cost.

Retention strength — specialists solving specific problems well achieve stronger retention than generalists solving many problems adequately. Legal tech retention metrics at focused companies often exceed category averages.

Market Dynamics Advantages

Legal tech market dynamics favor specialists:

Category ownership — specialists can own categories in buyer minds. When buyers think "contract AI," specialists who focus solely on contract AI achieve awareness that generalists cannot. Legal operations software buyers seek best-in-class solutions.

Partnership opportunity — specialists can partner with other specialists to create best-of-breed stacks. Generalists cannot partner because they compete with everyone. Legal services marketplace models enable specialist collaboration.

Acquisition premium — strategic acquirers pay premiums for category leaders. Specialists achieving category leadership attract acquisition interest that generalists don't. Alternative legal service providers and ALSP market growth create additional acquirer interest.

Investment clarity — investors can evaluate specialists against clear criteria. Generalists are harder to evaluate because success depends on execution across many dimensions. Legal tech investment opportunities are clearer for focused companies.

The Integration Tax

Integrated providers pay an integration tax that specialists avoid:

Coordination overhead — integrated providers must coordinate across product lines, creating overhead specialists don't bear. Law firm process automation attempts to reduce this tax but cannot eliminate it.

Compromise architecture — integrated platforms make architectural compromises to support diverse capabilities, resulting in suboptimal implementation of each

Resource competition — internal competition for resources creates politics and suboptimal allocation that specialists avoid

Customer confusion — integrated offerings confuse buyers about what the product actually does well versus adequately

The integration tax compounds over time, widening gaps between specialist and generalist capabilities in specific domains. The legal industry transformation favors specialists who avoid this tax.

Investment Strategy for Modular Legal Tech

The unbundling thesis implies specific legal tech investment strategies for identifying and capturing value. Understanding legal services market trends guides effective capital deployment.

Module Selection

Not all legal service modules offer equal investment opportunity:

Market size — modules must be large enough to support venture-scale outcomes. Some unbundled pieces, while valuable, address markets too small for venture returns. Legal tech market analysis must rigorously assess addressable market.

Growth trajectory — modules should be growing, ideally driven by secular trends (regulatory complexity, digital transformation, AI capability) rather than cyclical factors. The future of legal services lies in modules with sustained growth drivers.

Technology leverage — modules where technology creates substantial advantage over traditional delivery offer stronger investment theses than modules where technology adds marginal improvement. Scalable legal tech opportunities require technology-driven differentiation.

Competitive dynamics — modules with fragmented competition or clear paths to leadership offer better risk-adjusted returns than modules with entrenched leaders. Understanding law firms vs legal tech competitive dynamics matters.

Buyer readiness — modules where buyers are ready to purchase specialized solutions outperform modules where buyers still prefer bundled delivery. In-house legal technology adoption patterns signal buyer readiness.

Company Evaluation

Within attractive modules, legal tech startup evaluation should consider:

Specialization purity — companies focused purely on their module outperform those attempting adjacent expansion before achieving module dominance

Technical differentiation — sustainable competitive advantage requires technical capabilities competitors cannot easily replicate. API-based legal services architectures can create technical moats.

Go-to-market efficiency — efficient customer acquisition in the specific module indicates product-market fit and scaling potential. Legal tech unit economics must support efficient growth.

Team-market fit — teams with deep domain expertise in their specific module outperform generalist teams attempting to learn domains

Integration capability — despite specialization, successful products must integrate into customer workflows and technology stacks. Legal workflow automation requires seamless integration.

Portfolio Construction

Legal tech portfolio construction should reflect unbundling dynamics:

Module diversification — portfolios should span multiple modules to capture unbundling value across the legal services spectrum

Stage diversification — different modules are at different unbundling stages, requiring different stage focus

Thesis consistency — all investments should reflect the unbundling thesis, avoiding investments in integrated approaches that thesis suggests will underperform

Exit awareness — portfolio construction should consider exit paths, recognizing that specialists attract both strategic acquirers seeking capability and platforms seeking rebundling assets

According to analysis of vertical market software, specialized solutions often outperform horizontal alternatives in specific markets — a principle that applies directly to legal tech modules.

Timing Considerations

Legal tech investment timing should reflect module maturity:

Early unbundling — invest in specialists before categories establish clear leaders. Early investment captures value as categories develop.

Growth phase — invest in category leaders as they scale. Growth-phase investment captures expansion value with reduced early-stage risk.

Consolidation phase — invest in acquirers consolidating fragmented categories. Consolidation investment captures value as rebundling begins.

Platform phase — invest in platforms rebundling specialized capabilities. Platform-based legal services investment captures value from coordination layer above specialists.

Different modules are at different phases, enabling diversified timing exposure across portfolio.

Case Studies: Unbundling in Action

Examining how unbundling has proceeded in specific modules illustrates patterns and investment implications.

Case Study: E-Discovery Unbundling

E-discovery provides the clearest unbundling case study:

Pre-unbundling — law firms provided document review as part of litigation services, employing associate armies to review documents at hourly rates

Unbundling catalyst — technology enabling automated document processing created opportunity for specialized providers to deliver review faster and cheaper than firm-based approaches

Market development — e-discovery grew from service to technology category, with specialized vendors achieving scale and eventual public markets or strategic acquisition

Current state — e-discovery is mature, with established leaders and ongoing AI enhancement. The module successfully unbundled, validating the thesis.

Investment lessons — early e-discovery investors captured substantial returns. Current opportunity shifts to AI enhancement and adjacent module expansion.

Case Study: Contract Management Unbundling

Contract lifecycle management illustrates successful unbundling of operational legal functions:

Pre-unbundling — contracts lived in file cabinets and basic document management systems. Firms provided drafting but companies managed post-execution.

Unbundling catalyst — technology enabling contract repository, workflow, and analytics created opportunity for specialized CLM vendors

Market development — CLM emerged as major category, attracting significant venture investment and achieving substantial market penetration

Current state — CLM is maturing, with consolidation underway and AI enhancement creating next-generation capabilities

Investment lessons — CLM demonstrates that unbundled modules can achieve significant scale and attract substantial investment. Current opportunity involves AI enhancement players, vertical specialists targeting specific industries, and integration platforms connecting CLM with adjacent workflows.

Case Study: Legal Research Evolution

Legal research shows how unbundling evolves over time:

First unbundling — Westlaw and LexisNexis unbundled research from law libraries, creating technology-delivered research services

Re-unbundling — AI-powered research platforms are unbundling research from established database providers, offering capabilities legacy platforms cannot match

Current state — the module is experiencing second-wave unbundling as AI creates capability discontinuity

Investment lessons — modules can unbundle multiple times as technology advances. Monitoring technology discontinuities identifies re-unbundling opportunities.

The Rebundling Horizon

While current opportunity lies in unbundling, rebundling dynamics will eventually create different investment opportunities.

How Rebundling Occurs

Legal services rebundling will likely proceed through:

Platform aggregation — platforms that aggregate best-of-breed specialists, providing unified access and workflows while preserving specialist advantages

Workflow integration — solutions that connect unbundled modules into coherent workflows, capturing value from coordination rather than component delivery

Data network effects — platforms that accumulate data across modules, creating advantages that specialists cannot replicate independently

Customer convenience — offerings that simplify procurement and management for buyers overwhelmed by specialist complexity

When to Shift Focus

Investors should monitor signals indicating rebundling timing:

Buyer fatigue — when buyers express frustration with managing multiple specialist vendors, rebundling demand emerges

Integration standardization — when integration standards mature, platform players can aggregate specialists more easily

Market concentration — when modules develop clear leaders, rebundling can occur around established specialist positions

Platform emergence — when credible platform players emerge with aggregation capabilities and market positioning

Investment Implications

Rebundling investment opportunities will differ from unbundling opportunities:

Platform plays — investing in platforms that aggregate specialists rather than specialists themselves

Integration layer — investing in integration capabilities that connect unbundled modules

Data advantage — investing in companies accumulating cross-module data that creates network effects

Market timing — shifting from unbundling to rebundling investments as market dynamics evolve

Table 2: Unbundling vs. Rebundling Investment Characteristics

| Characteristic | Unbundling Phase | Rebundling Phase |

| Primary Target | Specialized module leaders | Integration platforms |

| Value Creation | Depth of capability | Breadth of coordination |

| Competitive Moat | Technical excellence in module | Network effects, data advantages |

| Exit Path | Strategic acquisition, category IPO | Platform scale, ecosystem dominance |

| Key Risk | Module market size limits | Execution complexity |

| Timing | Current (2020s) | Future (late 2020s-2030s) |

Author: Emily Radford;

Source: esmife.com

Risks and Challenges

The unbundling thesis carries risks that investors should evaluate:

Module Size Risk

Some unbundled modules may be too small for venture returns:

Addressable market limits — not every legal task represents sufficient market to support venture-scale companies. Some pieces, while valuable for customers, address markets too small for venture economics.

Winner-take-most dynamics — modules may support only one or two winners, limiting portfolio diversification. Legal tech market concentration in some modules may leave limited room for multiple successful players.

Adjacent competition — modules may face competition from adjacent markets that limits growth potential. Enterprise software players expanding into legal modules may compress opportunity for legal-focused specialists.

Regulatory barriers — some modules may face regulatory constraints that limit addressable market or require compliance investments that burden economics.

Careful module selection and market sizing mitigates size risk, but some modules will disappoint regardless of execution quality. Legal tech due diligence must rigorously assess module market potential.

Integration Complexity

Unbundled modules must integrate into customer environments:

Integration burden — customers tire of integrating multiple specialist solutions, potentially favoring integrated alternatives despite capability compromises

Workflow disruption — specialized solutions that don't fit existing workflows face adoption barriers

Data silos — unbundled modules may create data fragmentation that integrated solutions avoid

Investment should favor specialists with strong integration capabilities and partnerships that ease customer implementation.

Buyer Preference Risk

Buyers may not embrace unbundled purchasing:

Procurement convenience — some buyers prefer single vendors despite specialist advantages

Relationship preference — some buyers value firm relationships that bundled models provide

Risk concentration — buyers may perceive concentrated risk in bundled solutions as manageable versus distributed risk across specialists

Market segments vary in unbundling receptivity. Investment should target segments with demonstrated specialist adoption.

Premature Rebundling

Rebundling could occur faster than expected:

Platform acceleration — well-funded platforms could accelerate rebundling, compressing specialist value capture windows

Incumbent response — established players could rebundle more effectively than specialists anticipate

Buyer demand — buyer preference for rebundled solutions could emerge faster than module maturation allows

Monitoring rebundling signals and maintaining portfolio flexibility helps manage timing risk.

Conclusion: The Modular Legal Future

The unbundling of legal services represents a structural transformation creating substantial investment opportunity. The full-service law firm model that dominated for over a century is fragmenting into specialized components, each addressable by focused technology providers that outperform traditional bundled delivery.

The investment thesis is clear: modular legal tech specialists develop deeper capabilities, attract stronger talent, iterate faster, and achieve market positioning that integrated providers cannot match. The integration tax that generalists pay compounds over time, widening competitive gaps in specific domains. Buyers increasingly recognize specialist advantages and have sophistication to assemble best-of-breed solutions rather than accepting bundled compromises.

The opportunity spans multiple modules: legal research AI disrupting legacy platforms; legal drafting automationtransforming document creation; compliance technology managing regulatory complexity that manual approaches cannot address; dispute resolution platforms resolving conflicts more efficiently than traditional litigation; contract lifecycle management maturing while AI creates next-generation capabilities. Each module has distinct investment dynamics, enabling diversified exposure to unbundling value creation.

According to analysis of disintermediation, technology enabling direct connections between service providers and customers often disrupts intermediary institutions. Law firms have functioned as intermediaries bundling legal capabilities; unbundling is the disintermediation of that model.

For legal tech investors, the unbundling thesis provides clear framework for opportunity identification and evaluation. Module selection matters — not all pieces support venture-scale outcomes. Company evaluation should emphasize specialization purity, technical differentiation, and integration capability. Portfolio construction should span modules while maintaining thesis consistency. Timing awareness should balance current unbundling opportunity against eventual rebundling dynamics.

The unbundling thesis also carries implications beyond investment. For legal tech founders, it suggests building focused companies that excel at specific pieces rather than attempting to boil the ocean. For legal buyers, it suggests evaluating specialist solutions rather than defaulting to bundled firm services. For law firms, it suggests understanding which services face specialist competition and how to respond.

The modular legal future will look dramatically different from the bundled past. Services that seemed inseparable will operate independently. Capabilities that law firms monopolized will be available from specialized providers. Buyers who accepted bundled offerings will assemble custom solutions. And investors who recognize unbundling early will capture value as disaggregation proceeds.

The transition will not be instantaneous or uniform. Some modules will unbundle faster than others. Some buyers will adopt specialist solutions earlier than others. Some markets will embrace modular approaches more readily than others. But the direction is clear: the legal services industry is moving from bundled to modular, from integrated to specialized, from institutions to technology.

Legal tech investment positioned for this transition will capture returns as value shifts from traditional institutions to focused technology providers. The investors who recognized similar transitions in other industries — financial services, healthcare, media — and positioned appropriately generated substantial returns. The legal services transition is underway, and the investment opportunity is substantial.

The pieces are worth more than the whole — and investment strategy should reflect that reality. The modular legal future is being built by specialists who understand that depth beats breadth, focus beats dispersion, and excellence in one domain beats adequacy across many. The investment opportunity is to back those specialists as they capture value that unbundling creates.

Related Stories

Read more

Read more

The content on esmife.com is provided for general informational and educational purposes only. It is intended to present insights, trends, and examples related to investing in legal technology and should not be considered legal, financial, investment, or professional advice.

All information, materials, and references shared on this website are for general informational purposes only. Investment strategies, legal technologies, market conditions, and outcomes may vary based on individual circumstances and should be evaluated independently.

Esmife.com makes no representations or warranties regarding the accuracy, completeness, or reliability of the information provided and is not responsible for any errors or omissions, or for decisions made based on the content presented on this website.