The giants are watching legal tech.

Will Big Tech Enter Law? And What That Means for Legal Tech Investors

Introduction: The Looming Question

Every legal tech investor eventually confronts the same uncomfortable question: what happens if Big Tech decides to enter legal? The scenario haunts venture capitalists, startup founders, and private equity firms alike. Microsoft legal tech, Google legal technology, or Amazon legal tech could theoretically leverage their massive resources, AI capabilities, customer relationships, and distribution channels to capture legal technology market segments that took startups decades to develop.

The question isn't academic. Big tech legal tech interest has grown visibly in recent years. Microsoft's Copilot integrations increasingly touch legal workflows. Google's AI capabilities could transform legal research overnight. Amazon Web Services powers much of legal tech's infrastructure and could easily move up the stack. Each tech giant possesses resources that dwarf the entire legal tech market size — making big tech entering legal industry strategically feasible whenever they choose to prioritize it.

Yet the giants haven't made decisive moves into legal. Despite the market's size and apparent attractiveness, tech giants in legal industry involvement remains limited to infrastructure and productivity tools rather than purpose-built legal solutions. Understanding why — and whether that will change — is essential for anyone investing in, building, or acquiring legal technology companies. The big tech threat to legal SaaS remains theoretical but cannot be ignored.

The strategic calculus for legal tech investment depends heavily on Big Tech scenarios. If giants are likely to enter and dominate, investing in legal tech startups becomes a race against time — build value quickly and exit before legal tech market disruption arrives. If giants are unlikely to enter or likely to enter through acquisition, legal tech becomes more attractive — with potential for either independent growth or premium legal tech acquisition exits to Big Tech buyers.

"The Big Tech question is the elephant in every legal tech board room," observes a veteran legal tech venture capital investor. "We either need to believe they won't come, or we need to position our companies as acquisition targets rather than competition victims. There's no middle ground."

— Emily Radford

This analysis examines Big Tech's legal technology potential, the factors that have kept giants at bay, the scenarios that could trigger entry, and how legal tech investors should position for various outcomes — whether the legal tech vs big tech battle materializes or remains hypothetical.

Why Big Tech Could Dominate Legal

The big tech legal services potential is enormous. Understanding what makes tech giants potentially formidable legal tech competitors illuminates both the threat and the opportunity. The question of can big tech replace legal tech deserves serious analysis.

Unmatched AI Capabilities

The AI legal platforms revolution fundamentally favors organizations with AI capabilities at scale. Microsoft, Google, and Amazon have invested tens of billions in AI infrastructure, talent, and research — investments that legal tech companies cannot match individually or collectively. The AI capability gap between Big Tech and legal tech companies is not narrowing; it's widening.

The AI advantage manifests across multiple dimensions:

- Foundation models — Big Tech controls the large language models that power generative AI legal platforms. GPT (Microsoft/OpenAI), Gemini (Google), and Bedrock models (Amazon) provide capabilities that legal tech companies license rather than own. This creates fundamental dependency — legal tech companies build on foundations they don't control.

- Training data — Tech giants have access to training data at scales legal tech companies cannot approach. Google has indexed the internet; Microsoft has Office document data from billions of documents; Amazon has AWS customer data across thousands of enterprises. Legal-specific training could leverage these foundations to create enterprise AI legal software capabilities no legal tech company could match.

- AI talent — The engineers capable of building frontier AI systems work primarily at Big Tech companies that can pay premium compensation. Legal tech companies compete for talent Big Tech can outbid by factors of two or three. The talent concentration in Big Tech compounds over time as AI becomes more central to technology development.

- Compute infrastructure — Training and running AI models requires compute resources that Big Tech owns and legal tech companies rent. This cost structure disadvantage becomes more significant as cloud legal softwarecapabilities become central to competition. Big Tech can train models at costs legal tech companies cannot afford.

- Continuous improvement — Big Tech AI capabilities improve continuously through massive R&D investment. Legal tech companies building on these foundations must constantly adapt to changes they don't control. Platform risk SaaS vendors face is substantial when platforms evolve rapidly.

- Research leadership — Big Tech publishes frontier AI research and attracts academic talent that advances the field. Legal tech companies consume research rather than producing it, perpetually playing catch-up.

The Microsoft AI legal capabilities through Copilot already demonstrate how quickly Big Tech can bring AI to professional workflows. Similar capabilities purpose-built for legal could transform the market overnight. The question is whether Big Tech chooses to prioritize legal-specific AI development.

Distribution and Customer Relationships

Big Tech's existing customer relationships provide distribution advantages that legal tech companies spend years and fortunes attempting to build. The distribution moat is perhaps Big Tech's most underappreciated advantage in the vertical SaaS vs horizontal platforms competition:

Microsoft touches virtually every law firm and corporate legal department through Office 365, Teams, and Azure. Legal capabilities integrated into these enterprise legal software platforms would reach customers instantly without separate sales processes. Microsoft's enterprise sales teams already have relationships with legal technology buyers; adding legal products to their portfolios would leverage existing trust and access. The Microsoft 365 ecosystem represents the daily working environment for most legal professionals — adding legal capabilities there creates adoption paths that standalone vendors cannot match.

Google reaches legal professionals through Workspace, Search, and Chrome. Google's understanding of information retrieval — the foundation of legal research — provides natural adjacency to legal tech cloud platforms. Google's AI capabilities, particularly in natural language understanding and search, align closely with legal research and analysis use cases. The Google Cloud Platform serves enterprise customers who could adopt legal capabilities integrated into their existing cloud based legal management systems.

Amazon serves enterprise customers through AWS, which hosts significant portions of legal tech infrastructure. Amazon's B2B capabilities through AWS and its understanding of workflow automation could extend into cloud legal software. AWS already provides the infrastructure layer for many legal tech applications; moving up the stack into applications would leverage existing relationships and technical foundations. Amazon's experience with complex logistics and workflow optimization could translate into legal operations software enterprise management.

The enterprise legal technology sales cycles that consume years for startups could compress to months or weeks for Big Tech vendors adding capabilities to existing relationships. The customer acquisition cost advantage is dramatic — Big Tech can add legal capabilities to customers they already serve at marginal cost, while legal tech companies must build relationships from scratch at substantial expense through complex legal tech procurement processes.

The distribution advantage extends beyond direct sales to ecosystem effects. Big Tech platforms have marketplace and integration ecosystems where legal tech could be distributed to customers already engaged with the platform. This amplifies reach beyond direct sales relationships and creates ecosystem risk SaaS vendors must consider.

Capital and Patience

Big tech entering legal industry could be funded at scales that no legal tech company could survive competing against. A single tech giant could invest more in legal technology in one year than the entire VC investment legal tech ecosystem has invested over a decade.

This capital advantage enables strategies unavailable to smaller players and creates significant SaaS investment risk for current market participants:

Loss-leader pricing — Big Tech could offer legal capabilities at prices that destroy legal tech economics while remaining immaterial to their overall businesses. The platform dominance software playbook often includes aggressive pricing that smaller competitors cannot match.

Long-term investment — Big Tech can invest for years without profitability pressure that constrains venture-backed companies. The patience to build markets over decades rather than quarters provides strategic flexibility.

Acquisition capacity — Big Tech could acquire leading legal tech companies at valuations that provide attractive legal tech exits for investors while consolidating market position. The tech M&A strategy playbook includes acquiring market leaders to accelerate entry.

Talent acquisition — Big Tech could hire entire legal tech teams rather than competing with them, acquiring expertise through talent rather than company acquisition.

The legal tech market disruption potential from a well-funded Big Tech entry is existential for current market participants. The winner takes most SaaS dynamics that Big Tech entry could trigger would reshape competitive structure entirely.

Why Big Tech Hasn't Entered (Yet)

Despite apparent advantages, Big Tech in legal tech remains limited. Understanding the factors that have kept giants at bay helps assess whether those barriers will persist.

Market Size Relative to Big Tech Scale

The legal tech market size — perhaps $30-40 billion globally including services according to legal technology industry analysis — is significant but small relative to Big Tech's existing businesses and ambitions. Microsoft's annual revenue exceeds $200 billion; Google's exceeds $300 billion; Amazon's exceeds $500 billion. Legal tech represents a rounding error at Big Tech scale.

The market size calculation affects Big Tech decision-making in fundamental ways that shape strategic priorities:

Opportunity cost — resources devoted to legal could instead address markets ten or one hundred times larger. Big Tech prioritizes cloud infrastructure, AI platforms, advertising, and e-commerce over vertical markets like legal because the return on investment in larger markets exceeds what legal can offer.

Execution capacity — Big Tech has finite execution capacity despite vast resources. Adding legal technology requires management attention, product resources, and go-to-market investment that could deploy elsewhere with greater impact.

Return expectations — Big Tech shareholders expect growth at scale. A legal tech business that might be transformative for a startup barely moves the needle for a tech giant. Even capturing 100% of legal tech market would add less than 5% to any Big Tech company's revenue.

Strategic focus — Big Tech companies maintain strategic focus by avoiding vertical diversification that dilutes management attention. Legal represents exactly the kind of vertical complexity that Big Tech typically avoids.

The implication for legal tech investment thesis development: Big Tech may never prioritize legal because the opportunity cost of doing so exceeds the return from legal market capture. The market is attractive for focused players but insufficiently attractive for companies with trillion-dollar market opportunities elsewhere.

Regulatory and Professional Complexity

The legal industry presents regulatory complexity that tech giants have historically avoided. According to unauthorized practice of law regulations, providing legal services requires navigating professional responsibility obligations that technology companies are unaccustomed to:

Unauthorized practice of law — providing legal services without attorney involvement triggers professional regulations that vary by jurisdiction and remain actively enforced. Big Tech's standard playbook of "move fast and break things" doesn't work when the things being broken are professional licensing rules that carry civil and criminal penalties.

Professional responsibility — attorney ethical obligations create requirements around confidentiality, conflicts, and competence that technology products must navigate carefully. The Rules of Professional Conduct impose duties on attorneys that extend to the tools they use.

Malpractice exposure — AI-generated legal content that causes harm could create liability exposure that risk-averse Big Tech legal departments would resist. The malpractice insurance implications of AI-generated legal advice remain unsettled.

Regulatory capture resistance — bar associations and legal regulators have historically resisted technology disruption that threatens attorney economic interests. The regulatory environment is actively hostile to non-attorney legal service provision.

The tech companies legal services regulatory barrier has proven persistent. Big Tech has disrupted industries with less regulatory protection more readily than those with professional licensing requirements. Healthcare provides a cautionary analogue — despite massive investment, tech giants have struggled to disrupt healthcare delivery due to regulatory complexity.

Customer Complexity and Buying Patterns

Legal technology customers — law firms and corporate legal departments — present sales challenges that Big Tech's standard go-to-market approaches struggle with:

Conservative buyers — legal professionals adopt technology slowly and skeptically, preferring proven solutions over innovative alternatives. Big Tech's consumer-oriented brands may not resonate with conservative legal buyers.

Complex procurement — enterprise legal technology sales involve long cycles, multiple stakeholders, security reviews, and customization requirements that favor specialized vendors over generalists.

Relationship intensity — legal technology success requires implementation support, training, and ongoing customer success that Big Tech's scale-oriented models don't naturally provide.

Specialization expectations — legal buyers expect vendors to understand legal workflows deeply. Big Tech's horizontal orientation may read as superficial understanding of legal-specific needs.

The legal technology market barriers that frustrate startups also frustrate Big Tech. Market complexity that creates pain for small vendors doesn't automatically become easier for large ones.

Table 1: Big Tech Legal Entry — Advantages vs. Barriers

| Factor | Big Tech Advantage | Barrier to Entry |

| AI Capabilities | Unmatched AI resources and talent | Legal-specific training and expertise required |

| Distribution | Existing customer relationships | Legal buyers prefer specialized vendors |

| Capital | Unlimited investment capacity | Market size doesn't justify Big Tech focus |

| Scale | Ability to undercut on price | Legal margins don't fit Big Tech models |

| Brand | Consumer trust and recognition | Legal buyers skeptical of consumer brands |

| Regulation | Lobbying resources | UPL rules create real liability risk |

Author: Emily Radford;

Source: esmife.com

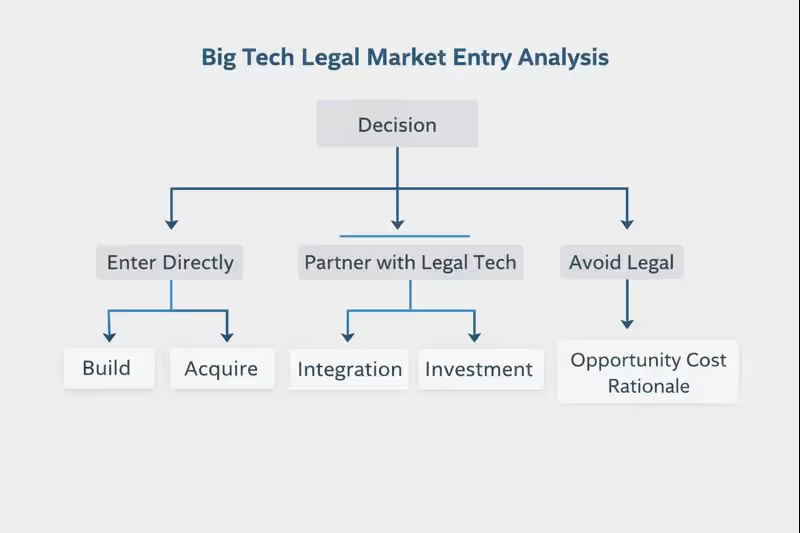

Scenarios for Big Tech Entry

The Big Tech legal technology question isn't binary. Multiple entry scenarios exist, each with different implications for legal tech investors and companies.

Scenario 1: Direct Entry Through Building

Big Tech could build legal-specific capabilities extending their existing platforms. This Microsoft legal software or Google legal platform scenario would involve:

Initial moves — enhanced legal-specific features in existing productivity tools, legal research capabilities in search platforms, or legal workflow automation in cloud services

Expansion — purpose-built legal applications that compete directly with legal tech vendors, leveraging AI capabilities and distribution advantages

Dominance — comprehensive legal platforms that make standalone legal tech tools unnecessary

Probability assessment: Low-to-medium in near term. The market size, regulatory complexity, and execution requirements make direct building less attractive than it appears. Big Tech would likely pursue this path only if legal became strategically important for broader reasons — AI demonstration, enterprise platform completion, or competitive response.

Implications for investors: Most threatening scenario. Direct Big Tech entry with building intent signals market disruption that could destroy legal tech value. Investors should monitor Big Tech legal hiring, product announcements, and strategic signals closely.

Scenario 2: Entry Through Acquisition

Big Tech could acquire leading legal tech companies rather than building capabilities internally. This Big Tech legal tech acquisition scenario represents the most attractive outcome for current investors:

Acquisition targets — market-leading platforms with strong customer relationships, differentiated technology, and strategic value

Valuation dynamics — Big Tech acquirers could pay premium multiples that venture and PE investors cannot match, creating attractive exit opportunities

Integration patterns — acquired companies would integrate into Big Tech platforms, potentially accelerating legal technology adoption through Big Tech distribution

Probability assessment: Medium-to-high over the long term. Acquisition is Big Tech's standard approach to entering specialized verticals. Legal tech acquisitions would be consistent with historical patterns if legal became strategic.

Implications for investors: Most attractive scenario. Building companies that could become Big Tech acquisition targets positions for premium exits. The legal tech exit strategy should include Big Tech acquisition as a possibility.

Scenario 3: Partnership and Integration

Big Tech could partner with legal tech companies rather than competing with them. This scenario involves:

Deep integration — legal tech companies building on Big Tech platforms with preferential access, co-development, and go-to-market support

Investment relationships — Big Tech strategic investments in legal tech companies that create alignment without full acquisition

Ecosystem development — Big Tech platforms creating marketplaces where legal tech companies can reach Big Tech customers

Probability assessment: High and already occurring. Microsoft, Google, and Amazon all have partnership programs that legal tech companies participate in. The question is whether partnerships deepen or give way to competition.

Implications for investors: Moderately positive scenario. Partnership creates value for legal tech companies without disruption risk, though it may limit ultimate exit valuations compared to acquisition.

Scenario 4: Continued Avoidance

Big Tech could continue treating legal as a vertical not worth prioritizing:

Maintained focus — Big Tech continues prioritizing cloud, AI platforms, consumer services, and larger enterprise verticals over legal-specific opportunities

Indirect participation — Big Tech captures value through infrastructure (Azure, AWS, GCP) and productivity tools (Office, Workspace) without competing in legal-specific categories

Acquisition disinterest — Big Tech acquirers remain focused on larger opportunities, leaving legal tech to venture and PE acquirers

Probability assessment: Significant probability in the near term. Current patterns suggest continued avoidance is the base case scenario.

Implications for investors: Status quo scenario. Legal tech competition remains among current players without Big Tech disruption, but also without Big Tech acquisition premiums.

Strategic Implications for Investors

The legal tech investment strategy must account for Big Tech scenarios across the investment lifecycle — from initial investment through exit. Understanding the build vs buy legal tech calculus that Big Tech faces helps inform positioning.

Investment Selection

Legal tech venture capital deployment should consider Big Tech scenarios in target selection:

Acquisition attractiveness — invest in companies that would be attractive Big Tech strategic buyers legal tech targets. This includes market leaders with strong customer relationships, differentiated technology with defensive moats, and strategic capabilities that Big Tech would want.

Defensibility — invest in companies with characteristics that would survive Big Tech entry. Deep specialization, regulatory advantages, customer intimacy, and network effects provide protection against software platform consolidation.

Platform compatibility — invest in companies positioned to benefit from Big Tech platform growth regardless of competitive dynamics. Building on Microsoft, Google, or Amazon platforms creates optionality for legal SaaS acquisition scenarios.

Avoid Big Tech collision courses — avoid investments that directly compete with Big Tech core capabilities. A legal research company competing with Google's information retrieval expertise faces asymmetric competitive risk in any legal tech vs big tech scenario.

The legal tech investor criteria should include explicit Big Tech scenario analysis for each potential investment, assessing both legal tech exit opportunities and competitive risk.

Portfolio Positioning

Private equity legal software and venture portfolio strategy should hedge across Big Tech scenarios:

Diversification — spread investments across companies with different Big Tech exposure profiles. Some companies would benefit from legal tech acquisition; others would benefit from Big Tech absence.

Timeline management — consider investment timelines that anticipate potential Big Tech moves. Earlier legal tech exits may be appropriate for companies most vulnerable to Big Tech competition.

Relationship development — cultivate relationships with Big Tech corporate development teams. Understanding Big Tech priorities helps anticipate moves and position portfolio companies for enterprise software exits accordingly.

Exit Strategy

The legal tech exit opportunities available depend heavily on Big Tech scenarios:

Big Tech acquisition exit — if Big Tech decides to enter through acquisition, portfolio companies that represent attractive targets could achieve premium legal tech M&A exits. Positioning companies as acquisition targets requires building characteristics Big Tech acquirers value.

Strategic acquirer exit — traditional strategic buyers legal tech (Thomson Reuters, Relativity, etc.) may accelerate acquisition activity if Big Tech threat increases, either to build scale for defense or to capture value before disruption.

PE exit — private equity legal software remains active in legal tech regardless of Big Tech scenarios, providing exit options through vertical SaaS consolidation for companies that may not attract strategic or Big Tech interest.

IPO exit — public market enterprise software exits become more complex in Big Tech entry scenarios. Investors considering IPO exits should assess how Big Tech narratives might affect public market receptivity and legal tech valuation.

"We underwrite every legal tech investment with explicit Big Tech scenarios," explains a legal tech-focused venture partner. "What happens if Microsoft decides to compete? What happens if Google decides to acquire? The investment has to make sense under multiple scenarios, not just the base case."

— Emily Radford

How Legal Tech Companies Should Position

Legal tech companies themselves — not just their investors — must develop Big Tech strategies that position for multiple outcomes.

Building Acquisition Attractiveness

Companies that could become Big Tech acquisition targets should cultivate characteristics that Big Tech acquirers value:

Market leadership — Big Tech acquires leaders, not also-rans. Companies should pursue category leadership that makes them obvious acquisition targets.

Strategic capabilities — develop capabilities that Big Tech would want but struggles to build internally. Legal-specific AI training data, regulatory expertise, and customer relationships provide strategic value.

Platform compatibility — ensure technology can integrate with Big Tech platforms without complete rebuilding. Modern architectures and API-first approaches increase acquisition attractiveness.

Clean operations — Big Tech acquirers prefer companies without legal, regulatory, or operational problems that complicate integration. Clean cap tables, clear IP ownership, and compliant operations matter.

Building Competitive Defensibility

Companies that may need to survive Big Tech competition should develop defensive characteristics:

Customer intimacy — deep customer relationships that survive competitive entry. Customers who view vendors as partners rather than tools are less likely to switch.

Specialized expertise — capabilities so legal-specific that Big Tech's horizontal approach cannot easily replicate them.

Regulatory positioning — business models and capabilities aligned with legal regulatory requirements that Big Tech may struggle to satisfy.

Network effects — business models that become more valuable with scale in ways that new entrants cannot easily overcome.

Platform Strategy

All legal tech companies should develop explicit Big Tech platform strategy:

Multi-platform positioning — avoid exclusive dependence on any single Big Tech platform. Companies dependent on Microsoft, Google, or Amazon face risk if those relationships change. Research on legal operations indicates that legal departments increasingly value vendor flexibility and platform independence.

Partnership cultivation — actively develop relationships with Big Tech platform teams. Understanding platform roadmaps helps anticipate changes and position accordingly.

Integration depth — deep integration with Big Tech platforms creates value but also creates switching costs. Balance integration benefits against dependency risks.

Optionality preservation — maintain architectural flexibility to shift platform dependencies if competitive dynamics require.

Table 2: Legal Tech Positioning Strategy by Big Tech Scenario

| Scenario | Investor Strategy | Company Strategy | Exit Implications |

| Direct Entry (Build) | Accelerate exits, avoid collision courses | Build defensibility, deepen customer relationships | Exit before disruption, strategic premiums |

| Entry via Acquisition | Position as acquisition targets | Maximize acquisition attractiveness | Premium Big Tech exits possible |

| Partnership Model | Invest in platform ecosystem leaders | Deepen platform integration | Moderate exits through traditional routes |

| Continued Avoidance | Standard legal tech investing | Standard competitive strategy | Traditional strategic/PE exits |

Author: Emily Radford;

Source: esmife.com

The Most Likely Path Forward

Predicting Big Tech legal tech strategy with certainty is impossible, but analysis of incentives and patterns suggests likely trajectories.

Near-Term Probability: Continued Limited Engagement

The most probable near-term scenario is continued Big Tech limited engagement with legal technology:

Infrastructure focus — Microsoft Azure, Google Cloud, and AWS continue serving legal tech infrastructure needs without competing in application layers

Productivity tool enhancement — Copilot and similar capabilities continue improving legal workflows within general productivity tools without becoming legal-specific applications

Selective partnerships — Big Tech continues partnering with legal tech companies for specialized capabilities without acquiring or competing with them

No major acquisition — absent strategic trigger, Big Tech likely continues prioritizing larger opportunities over legal tech acquisitions

This scenario is positive for current legal tech investors and companies. Competition remains among current players without Big Tech disruption. The window for building value and achieving exits remains open.

Medium-Term Catalyst: AI Demonstration Needs

The most likely catalyst for increased Big Tech legal engagement is AI demonstration:

Legal as AI showcase — legal work is knowledge-intensive and high-value, making it an attractive showcase for AI capabilities. Big Tech may pursue legal more aggressively to demonstrate AI potential.

Competitive pressure — if one tech giant makes significant legal moves, others may follow to avoid ceding strategic ground.

Enterprise AI strategy — as Big Tech competes for enterprise AI spending, legal-specific capabilities may become strategically important for enterprise sales.

AI-driven entry would likely come through enhanced capabilities and partnerships initially, with acquisition possible for companies that demonstrate AI leadership.

Long-Term Possibility: Acquisition Wave

If Big Tech decides legal is strategically important, acquisition is the most likely entry mechanism:

Faster than building — acquisition provides immediate capabilities, customer relationships, and market position that building would take years to develop

Risk reduction — acquiring proven companies reduces execution risk compared to building in unfamiliar markets

Talent acquisition — buying companies acquires teams with legal technology expertise that would be difficult to assemble

Historical precedent — Big Tech has used acquisition to enter specialized verticals consistently; legal would follow the pattern

An acquisition wave would create premium exit opportunities for well-positioned legal tech companies while consolidating the market around Big Tech platforms.

Frequently Asked Questions (FAQ)

1. Why haven't Microsoft, Google, or Amazon entered legal tech more aggressively?

Big tech legal tech entry has been limited by several factors: market size relative to Big Tech scale (legal tech is too small to move the needle), regulatory complexity (unauthorized practice of law rules create real liability risk), customer complexity (legal buyers are conservative and prefer specialized vendors), and opportunity cost (resources devoted to legal could address larger markets). These barriers have kept tech giants in legal industry involvement focused on cloud legal software infrastructure and productivity tools rather than purpose-built legal applications. The legal technology market remains attractive for focused players but insufficiently attractive for companies with trillion-dollar opportunities elsewhere.

2. What would trigger Big Tech to enter legal tech more aggressively?

The most likely triggers for big tech entering legal industry include: AI demonstration needs (legal as a showcase for generative AI legal platforms capabilities), competitive response (one giant's entry prompting others to follow), enterprise strategy requirements (legal capabilities needed to win broader enterprise AI legal software business), or strategic acquisition opportunity (a compelling legal tech acquisition target becoming available). Absent these triggers, continued limited engagement remains the base case for cloud providers legal software strategies.

3. Should legal tech investors be worried about Big Tech competition?

Legal tech venture capital investors should be aware but not paralyzed by Big Tech scenarios. The probability of direct legal tech market disruption that destroys value is low in the near term. More likely scenarios — legal tech M&A or partnership — could create value for well-positioned companies. Investors should select investments that would be attractive strategic buyers legal tech targets while also having defensibility characteristics that would survive platform dominance software competition. Explicit Big Tech scenario analysis should be part of every legal tech investmentthesis to manage SaaS investment risk.

4. How should legal tech companies position for potential Big Tech entry?

Legal tech companies should pursue dual-track positioning: building characteristics that make them attractive legal tech acquisition targets (market leadership, strategic capabilities, platform compatibility) while also developing defensibility that would survive the big tech threat to legal SaaS (customer intimacy, specialized expertise, regulatory advantages, network effects). Companies should develop explicit platform strategies for their legal ops technology stack that balance integration benefits against ecosystem risk SaaS dependency, maintaining optionality to shift positioning if Big Tech dynamics change.

5. Could Big Tech entry actually benefit legal tech investors?

Yes — legal tech M&A scenarios involving Big Tech could create premium legal tech exit opportunities for investors. Big Tech acquirers can pay legal tech valuation multiples that strategic and PE acquirers cannot match, and they have historically paid premiums for market-leading companies in vertical markets they decide to enter through tech M&A strategy. The enterprise software exits in a Big Tech acquisition scenario could exceed returns from traditional exits. The key is positioning portfolio companies as attractive acquisition targets while maintaining optionality for other outcomes in vertical SaaS consolidation scenarios.

Conclusion: Living with Uncertainty

The Big Tech legal technology question will remain unanswered until Big Tech decides to answer it — and that decision lies outside the control of legal tech investors, companies, or customers. The uncertainty is uncomfortable but manageable through strategic positioning that accounts for multiple scenarios.

The most likely near-term scenario — continued limited Big Tech engagement — provides runway for legal tech companies to build value and for investors to generate returns through traditional strategies. The window remains open, and the barriers that have kept Big Tech at bay appear persistent rather than temporary. Legal tech companies should use this window to build durable value rather than assuming it will remain open indefinitely.

The medium-term scenarios that could increase Big Tech engagement — AI demonstration, competitive response, enterprise strategy — would likely manifest initially through enhanced partnerships and integration rather than direct competition. This evolution would create opportunities for well-positioned legal tech companies to benefit from Big Tech platform growth while preparing for potential competitive scenarios.

The long-term possibility of significant Big Tech entry — most likely through acquisition — represents both threat and opportunity. Companies positioned as attractive acquisition targets could achieve premium exits that generate exceptional investor returns. Those positioned for defensibility could survive and potentially thrive in a market where Big Tech participation validates the opportunity and expands the addressable market.

For legal tech investors, the strategic imperative is portfolio construction and positioning that generates returns across scenarios. Investments should make sense whether Big Tech enters aggressively, enters through acquisition, deepens partnerships, or continues avoiding legal. The companies most likely to succeed — and most attractive as investments — are those building genuine value for customers rather than those merely hoping to avoid Big Tech attention. The legal tech investment strategy that works is one that doesn't depend on predicting Big Tech decisions accurately.

For legal tech companies, the imperative is building businesses that succeed regardless of Big Tech decisions. Customer value, operational excellence, and strategic positioning matter more than Big Tech speculation. Companies that build strong businesses position themselves well for any outcome; those that obsess over Big Tech scenarios while neglecting fundamentals position themselves poorly for all outcomes. The best defense against Big Tech competition is the same as the best preparation for Big Tech acquisition: building a company worth having.

The historical pattern across technology markets suggests that Big Tech eventually participates in markets that reach sufficient scale and strategic importance. Legal technology may not yet meet those thresholds, but it's approaching them. The AI transformation that makes legal technology more valuable also makes it more attractive to Big Tech. The market participants who thrive will be those who build value that matters regardless of what the giants decide — while remaining strategically aware enough to capitalize when decisions come.

The giants are watching legal tech. They may enter, they may acquire, they may partner, or they may continue watching. The legal tech market participants who thrive will be those who build value that matters regardless of what the giants decide — creating companies worth acquiring if Big Tech comes, and companies worth owning if Big Tech stays away.

Related Stories

Read more

Read more

The content on esmife.com is provided for general informational and educational purposes only. It is intended to present insights, trends, and examples related to investing in legal technology and should not be considered legal, financial, investment, or professional advice.

All information, materials, and references shared on this website are for general informational purposes only. Investment strategies, legal technologies, market conditions, and outcomes may vary based on individual circumstances and should be evaluated independently.

Esmife.com makes no representations or warranties regarding the accuracy, completeness, or reliability of the information provided and is not responsible for any errors or omissions, or for decisions made based on the content presented on this website.